Income Tax and Capital Gains Rates 2017

Money Matters – Skloff Financial Group Question of the Month – April 1, 2017

By Aaron Skloff, AIF, CFA, MBA

Q: Our taxes are confusing. What are the income tax rates, capital gains rates and how do they differ in 2017?

The Problem – Maze of Tax Rates on Income and Capital Gains

Not all sources of your income are the same in the eyes of the IRS. The IRS treats your wages differently than income you earn on your investments. The IRS also treats interest on your savings account and bonds differently than dividends on your stocks and funds, and the gains you realize on your stocks and funds. This creates a ‘maze’ of different rates for different circumstances.

The Solution – A Map for the Maze of Tax Rates on Income and Capital Gains

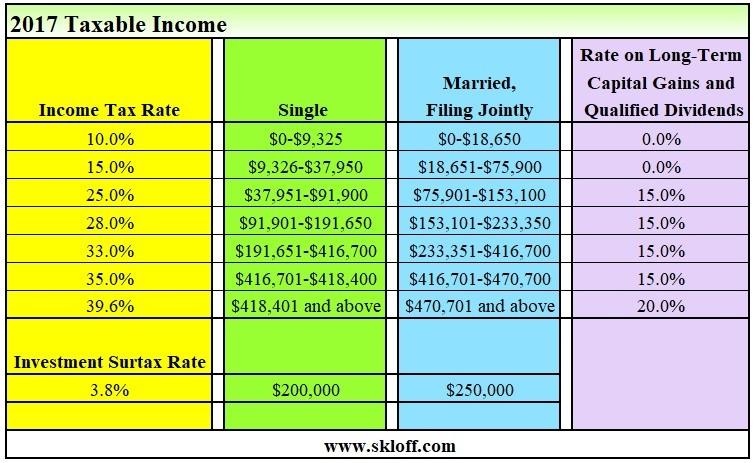

There are a number of factors that could impact the taxes you pay on your income and investments. The following table provides income tax and capital gains rates for single filers and those married, filing jointly.

Click to Enlarge

Income and Income Taxes

For many taxpayers, their primary source of income is their wages. For others, it may be pension or social security income and/or retirement account withdrawals (RMDs or otherwise). Others may rely on savings account and bond interest. Most taxpayers can aggregate income from wages, pensions, social security and interest to determine their total income. Your total taxable income can be impacted by a number of factors, including, but not limited to: alimony payments, contributions to employer retirement plans and/or IRAs, contributions to HSAs, exemptions, dependents, deductions (standard or itemized) and credits. These adjustments to your income result in your taxable income.

Although the top marginal income tax rate of 39.6% is assessed on taxpayers with taxable income of $418,401 and higher for single filers and $470,701 and higher for married couples filing jointly, the actual tax rate paid is the effective income tax rate. The effective income tax rate is the blended rate you actually pay. Based on the table above, a single filer earning $91,900 would have a top marginal income tax rate of 25% and an effective income tax rate of approximately 20%. The first $9,325 of income would be taxed at 10%, the next $28,625 (from $9,326 to $37,950) would be taxed at 15% and the last $53,950 (from $37,951 to $91,000) would be taxed at 25%.

Capital Gains and Qualified Dividends

Many taxpayers also own stocks, bond, mutual funds, exchange traded funds and other investments. If you receive a qualified dividend or buy and sell an investment for a gain outside of a tax sheltered account, you may be subject to a qualified dividend tax or capital gains tax. Short term capital gains (365 days or less) are taxed at ordinary income tax rates. Long term capital gains (366 days or more) are taxed at the rates in the table above. For example, single filer earning $37,950 would have a 0% qualified dividend rate and a 0% long term care gains rate.

Investment Surtax

Single filers with taxable income of $200,000 or higher and those married filing jointly with taxable income of $250,000 or higher are further penalized with an investment surtax (net investment income tax). The investment surtax rate is 3.8% on income from investments, including, but not limited to: interest, dividends, short and long-term capital gains, rental income, royalty income and passive business income.

Action Steps

With a map for the maze of income taxes and capital gains taxes, you can better prepare yourself for the 2018 tax season. Work closely with your Registered Investment Adviser (RIA) and tax professional throughout 2017 to optimize all the factors that impact your taxes.

Aaron Skloff, Accredited Investment Fiduciary (AIF), Chartered Financial Analyst (CFA), Master of Business Administration (MBA) is CEO of Skloff Financial Group, a Registered Investment Advisory firm. He can be contacted at www.skloff.com or 908-464-3060.

![]()

Are You Interested in Learning More?