Pacific PremierCare Choice MAX Hybrid Life and Long Term Care Insurance Review – Long Term Care University

Long Term Care University – Question of the Month – 04/01/21

By Aaron Skloff, AIF, CFA, MBA

Q: We read the Long Term Care University article that compares Traditional to Hybrid-Combination Life and Long Term Care (LTC) Insurance and prefer the Hybrid-Combination LTC policy. Can you please review the Pacific PremierCare Choice MAX Hybrid LTC policy?

Overview. Pacific Life Insurance Company is an A.M. Best A+ rated, founded in 1868. The Pacific PremierCare Choice MAX policy is a Hybrid Life and Long Term Care Insurance (also called Combination or asset based) policy. With Traditional LTC policies, premiums can be increased and you may not receive any benefits if you do not need LTC. With Hybrid LTC policies the benefits and premiums are guaranteed. The insurance company either: 1) pays you if you need LTC, 2) pays your heirs if you do not need LTC, 3) pays you and your heirs if you need a modest amount of LTC or 4) pays you a refund if you cancel the policy.

Click Here for Your Long Term Care Insurance Quotes

Pacific PremierCare Choice MAX is Unique Because It Does Not Have an Elimination Period for Home Care Reimbursements. Like a deductible on an automobile or homeowners insurance policy, an elimination period on a LTC insurance policy shifts the initial cost of a claim to you and away from the insurance company. An elimination period is the number of days you are responsible for paying for your LTC costs out of your own pocket. Pacific PremierCare Choice MAX has 0 day elimination for home and a 90 day elimination period for facility care if you choose to be reimbursed for your care expenses. If you choose the cash indemnity payment method both elimination periods are 90 days.

Pacific PremierCare Choice MAX is Unique Because It Offers Reimbursement or an 80% Cash Indemnity Option. There are two primary benefit payment methods among LTC policies. Reimbursement policies, the most common type of policies, require you to submit documentation of all expenses for reimbursement up to your monthly LTC benefits. Cash Indemnity policies pay up to your monthly LTC benefits, regardless of your expenses. The irreversible 80% cash indemnity option caps monthly and total LTC benefits at 80%.

Pacific PremierCare Choice MAX Policy Options. The policy options include: Benefit periods of 3-8 years; Inflation protection of none, 3% simple, 5% simple and 5% compound; Elimination period of zero days for home care and 90 days for other care or 90 days for both if 80% cash indemnity option is selected at time of claim; Reimbursement based benefit payment method; Refund of premium options: 1. 100% or 2. vesting schedule: 70% years 1-10, 76% year 11, 82% year 12, 88% year 13, 94% year 14, 100% year 15.

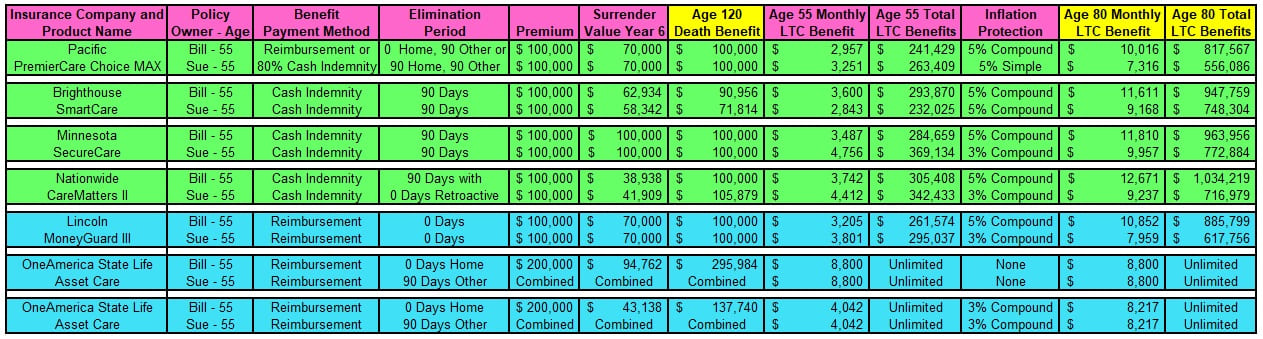

How Pacific PremierCare Choice MAX Compares with Other Hybrid LTC Policies. Let’s look at a husband and wife, Bill and Sue, who are each 55 years old and reside in New Jersey. They each pay a $100,000 one-time premium ($200,000 combined with State Life) and are expected to need LTC in 25 years at the age of 80. They are comparing Hybrid policies that offer the largest LTC benefits, with six years of LTC and inflation protection included in the premium (unless noted otherwise). They prefer Cash Indemnity (reimbursement policies in blue, cash indemnity policies in green in the chart below).

Pacific PremierCare Choice MAX Underperforms Most Competitors on a Cash Indemnity Basis with Lower Monthly and Total LTC Benefits. Bill will have $10,016 monthly and $817,567 total LTC benefits, while Sue will have $7,316 and $556,086, respectively. Brighthouse SmartCare is notable for its option to link policy values to major market indices. Lincoln MoneyGuard III is a strong alternative due to its 0 day elimination period. Minnesota Life Securian SecureCare is a strong cash indemnity alternative for Bill and Sue due to its higher monthly benefit and total LTC benefits. Nationwide Care Matters II is a strong cash indemnity alternative for Bill and Sue due to its higher monthly and total LTC benefits and its 90 day with 0 day retroactive elimination period. OneAmerica State Life Asset Care is a strong alternative due to its unlimited, lifetime total LTC benefits.

Click to Enlarge

Action Steps and Conclusions. Pacific PremierCare Choice MAX has relatively low monthly and total LTC benefits. The cash indemnity option allows for the use of formal and informal care providers. Since premiums vary greatly based on age, health and marital status, request individualized quotes.

Aaron Skloff, Accredited Investment Fiduciary (AIF), Chartered Financial Analyst (CFA) charter holder, Master of Business Administration (MBA), is the Chief Executive Officer of Skloff Financial Group, a Registered Investment Advisory firm. The firm specializes in financial planning and investment management services for high net worth individuals and benefits for small to middle sized companies. He can be contacted at www.skloff.com or 908-464-3060.

![]()