Does Your State Tax Pre-Tax Contributions to Retirement Accounts? – Part 2

Money Matters – Skloff Financial Group Question of the Month – June 1, 2025

By Aaron Skloff, AIF, CFA, MBA

Q: We read ‘Pre-tax Versus Roth Employer Contributions to Retirement Accounts – Which Is Better?’ Part 1 and Part 2 and ‘Does Your State Tax Pre-Tax Contributions to Retirement Accounts?’ Part 1. For state income tax purposes, which is more advantageous when contributing to and withdrawing from retirement accounts: pre-tax or Roth contributions?

The Problem – Determining if Pre-tax Contributions or Roth Contributions Are Better

Contributions to pre-tax retirement accounts are subject to state income taxes in some states. Withdrawals of pre-tax retirement account contributions are subject to state income taxes in some states. Withdrawals of Roth retirement account contributions are tax-free. Since tax-free withdrawals are better than taxable withdrawals, Roth contributions must be the simple answer to the question – right? Not so fast.

The Solution – Understanding the Advantages and Disadvantages of Pre-tax and Roth Contributions and Withdrawals

Both types of contributions have advantages and disadvantages upon contribution and withdrawal. Let’s examine them below.

Are You Interested in Learning More?

Pre-Tax Contributions

Advantages. Pre-tax contributions defer federal income taxes and state income taxes in some states, but are taxable in some states. For example: If you are in the 6% state (marginal) income tax rate, every $1.00 of pre-tax contributions defers $0.06 of taxes in some states.

Disadvantages. Pre-tax withdrawals are taxed at your state (marginal) income tax rate in some states. A disadvantageous example: If you will be in the 12% state (marginal) income tax rate when you take withdrawals in retirement, every $1.00 of pre-tax withdrawals will be subject to $0.12 of state income taxes. A common example: If you will be in the 10% state (marginal) income tax rate when you take withdrawals in retirement, every $1.00 of pre-tax withdrawals will only be subject to $0.10 of taxes.

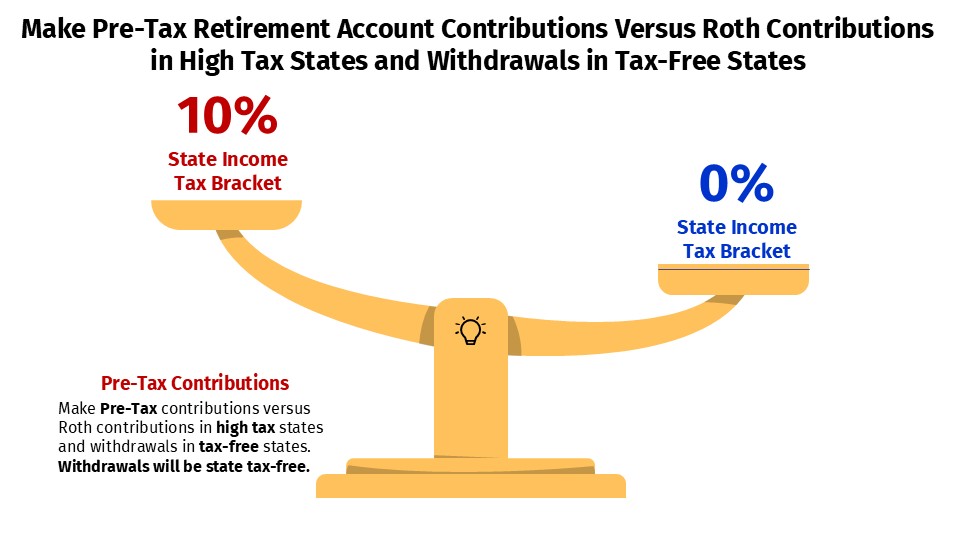

Strategy. Make pre-tax contributions instead of Roth contributions if your current state (marginal) income rate is higher than your future state (marginal) income tax rate. Contributing at a 10% pre-tax rate and withdrawing at a 0% rate creates a 10% tax arbitrage. See the chart below.

Click to Enlarge

Roth Contributions

Advantages. Roth contributions are subject to federal income taxes and state income taxes in some states, but are tax-free in some states. For example: If you are in the 12% state (marginal) income rate, every $1.00 of Roth contributions is subject to $0.12 of taxes. Lower income earners, such as younger employees, can utilize their full ‘low’ state (marginal) income tax rate as an arbitrage to a higher state (marginal) income tax rate on withdrawals in retirement.

Disadvantages. Roth withdrawals are tax-free. A disadvantageous example: If you will be in the 2% state (marginal) income tax rate when you take withdrawals in retirement, every $1.00 of Roth withdrawals will only avoid $0.02 of taxes. A common example: If you will be in the 10% state (marginal) income tax rate when you take withdrawals in retirement, every $1.00 of Roth withdrawals will avoid $0.10 of taxes.

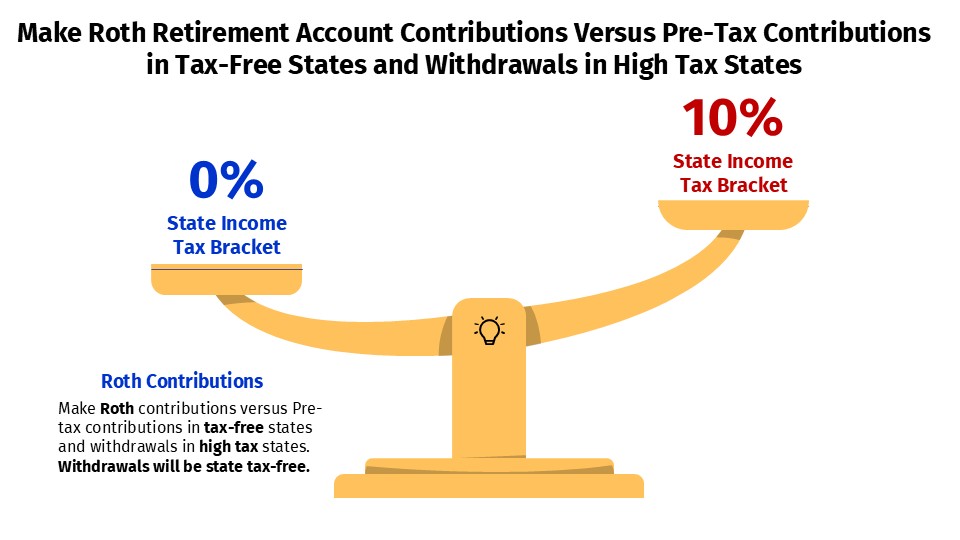

Strategy. Make Roth contributions instead of pre-tax contributions if your current state (marginal) income tax bracket is lower than your future state (marginal) income tax rate. Contributing at a 0% tax-free state (marginal) income tax rate and withdrawing, while avoiding a 10% state (marginal) income tax rate creates a 10% tax arbitrage. See the chart below.

Click to Enlarge

Action Steps

Realize tax arbitrage by deferring taxes with pre-tax contributions if your current income tax rate is higher than your future income tax rate. Realize tax arbitrage by paying taxes today with Roth contributions if your future income tax rate is higher than your current income tax rate. Work closely with your Registered Investment Adviser (RIA) to reduce your taxes, and grow and preserve your wealth.

Aaron Skloff, Accredited Investment Fiduciary (AIF), Chartered Financial Analyst (CFA), Master of Business Administration (MBA) is CEO of Skloff Financial Group, a Registered Investment Advisory firm specializing in financial planning, investment management and benefits for small to middle sized companies. He can be contacted at www.skloff.com or 908-464-3060.

![]()

Are You Interested in Learning More?