Investment Options

The Meta 401(k) offers a traditional mutual fund lineup and Fidelity BrokerageLink. Fidelity BrokerageLink provides thousands of investment options, allowing you to have your Meta 401(k) account professionally managed.

Professionally managed accounts can generate 3% to 4% higher returns per year.

Have Your Meta 401(k) Account Professionally Managed

2026 Contribution Limits

| Under age 50 | $24,500 |

| Ages 50-59 or 64+ | $32,500 [$24,500 + $8,000 catch-up] |

| Ages 60-63 | $35,750 [$24,500 + $11,250 catch-up] |

Pre-tax Contributions and Pre-Tax Catch-up Contributions

With pre-tax contributions and pre-tax catch-up contributions, you defer income taxes until you withdraw the assets.

Roth Contributions and Roth Catch-up Contributions

With Roth contributions and Roth catch-up contributions, you pay taxes on the contributions but withdrawals are tax-free.

Meta Match

Meta matches 50% on your contributions up to $24,500 of contributions in 2026 for ages under 50, resulting in a maximum match of $12,250 in 2026. Meta matches 50% on your contributions up to $32,500 of contributions in 2026 for ages 50-59 or 64+, resulting in a maximum match of $16,250 in 2026. Meta matches 50% on your contributions up to $35,750 of contributions in 2026 for ages 60-63, resulting in a maximum match of $17,875 in 2026. Meta matches catch-up contributions.

You must contribute $24,500 to receive your full match for ages under 50. You must contribute $32,500 to receive your full match for ages 50-59 or 64+. You must contribute $35,750 to receive your full match for ages 60-63.

Meta matches vest immediately.

Meta Match Examples

Employee Contributes $10,000

Based on a $360,000 salary, you contribute $10,000. Meta will match your contribution by 50% or $5,000.

Employee Contributes 6% of Salary

Based on a $360,000 salary, you contribute $21,600. Meta will match your contribution by 50% or $10,800.

Mega Backdoor Roth

In addition to your pre-tax and Roth contributions and the Meta match, you can utilize a Mega Backdoor Roth. You can contribute after-tax to your 401(k) up to the limit of all employee and employer contributions, then convert those after-tax contributions to a Roth IRA or Roth 401(k).

2026 Contribution Limits for All Employee and Employer Contributions

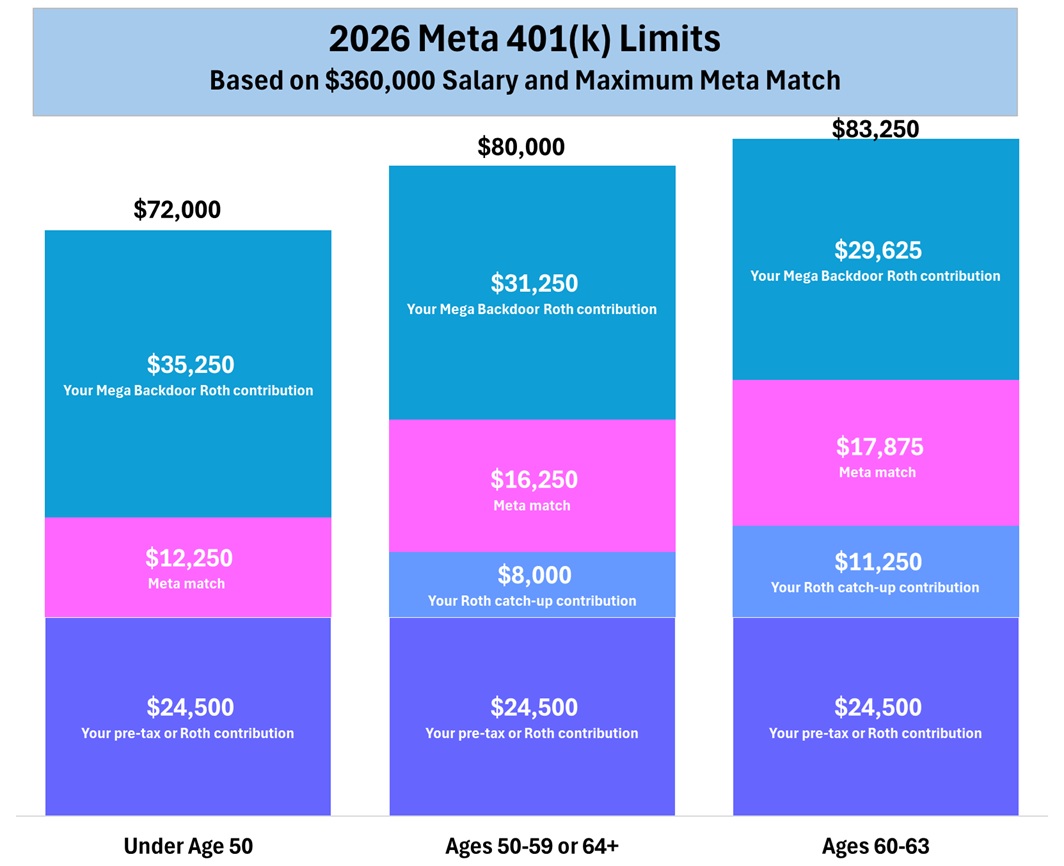

| Under age 50 | $72,000 |

| Ages 50-59 or 64+ | $80,000 |

| Ages 60-63 | $83,250 |

Mega Backdoor Roth Examples

Employee Under the Age of 50

Based on a $360,000 salary, you can generate $70,000 in 401(k) contributions. In addition to your pre-tax or Roth contributions and your Meta match, you can contribute $35,250 after taxes.

| Your pre-tax or Roth contributions | $24,500 |

| Meta match | $12,250 |

| Your Mega Backdoor Roth contributions | $35,250 |

| Total | $72,000 |

Employee Age 50-59 or 64+

Based on a $360,000 salary, you can generate $80,000 in 401(k) contributions. In addition to your pre-tax or Roth contributions and your Meta match, you can contribute $31,250 after taxes.

Starting in 2026, if your wages from the preceding year (2025) exceeded $145,000 (indexed to $150,000–$160,000 depending on final IRS inflation adjustments, though $145,000 is the base threshold), any catch-up contributions must be made on a Roth basis.

| Your pre-tax or Roth contributions | $24,500 |

| Your Roth catch-up contributions | $8,000 |

| Meta match | $16,250 |

| Your Mega Backdoor Roth contributions | $31,250 |

| Total | $80,000 |

Employee Age 60-63

Based on a $360,000 salary, you can generate $83,250 in 401(k) contributions. In addition to your pre-tax or Roth contributions and your Meta match, you can contribute $29,625 after taxes.

Starting in 2026, if your wages from the preceding year (2025) exceeded $145,000 (indexed to $150,000–$160,000 depending on final IRS inflation adjustments, though $145,000 is the base threshold), any catch-up contributions must be made on a Roth basis.

| Your pre-tax or Roth contributions | $24,500 |

| Your Roth catch-up contributions | $11,250 |

| Meta match | $17,875 |

| Your Mega Backdoor Roth contributions | $29,625 |

| Total | $83,250 |

Have Your Meta 401(k) Account Professionally Managed

Meta and Skloff Financial Group are not affiliated companies. While we make efforts to keep the information accurate, we make no guarantees. Please contact your benefits department to verify the information.