Are Indexed Universal Life (IUL) Insurance Policies as Good as They Sound? – Part 2

Money Matters – Skloff Financial Group Question of the Month – August 1, 2020

By Aaron Skloff, AIF, CFA, MBA

Q: We read the article ‘Are Indexed Universal Life Insurance Policies as Good as They Sound?’ Part 1. Can Indexed Universal Life (IUL) Insurance Policies be designed to maximize the tax-free death benefit?

The Problem – Maximizing the Tax-Free Death Benefit on Indexed Universal Life (IUL) Insurance Policies

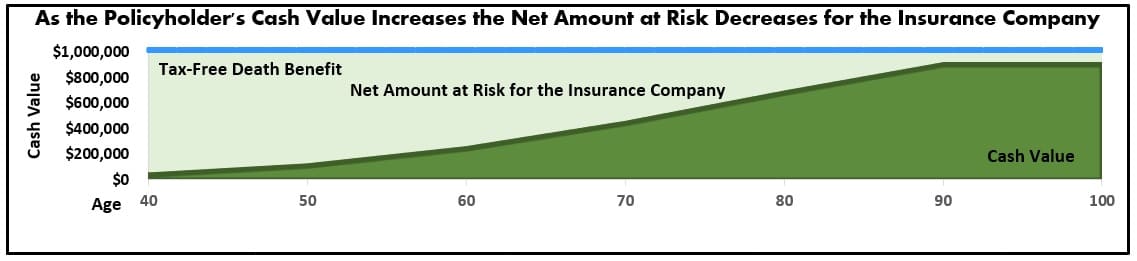

Indexed Universal Life (IUL) insurance policies must be customized to maximize tax-free death benefits.

Click Here for Your Life Insurance Quotes

The Solution – Customizing Indexed Universal Life (IUL) Insurance Policies to Maximize the Tax-Free Death Benefit

IUL insurance policies can be customized for various goals. If the goal is to maximize the tax-free death benefit, you can contribute to the policy beyond the premium for the tax-free death benefit. Those additional contributions are added to the cash value of the policy. The cash value increases with the indexed interest rate (credit rate), net of costs and charges, and can cover premiums and charges. The difference between the tax-free death benefit and cash value of the policy is the net amount at risk for the insurance company. See the chart below.

Click to Enlarge

Numbers Speak Louder Than Words. Let’s look at a husband and wife, Bill and Sue, who are each 40 years old. They each pay $10,000 per year for 25 years for IUL insurance policies. Their goal is to maximize their tax-free death benefit through age 100, while completing their premiums payments at age 64. The IUL policy they purchase receives credits annually based on the annual point-to-point price increase in the S&P 500 Index, is based on a 5.92% interest rate, 100% participation rate and a 9.50% cap on the S&P 500 Index.

Bill will have $1,766,123 of tax-free death benefit through age 100, despite paying $250,000 in cumulative premiums (highlighted in blue in the chart below). Had Bill paid the same premiums for a Guaranteed Indexed Universal Life Insurance (GIUL) policy or a Guaranteed Universal Life Insurance (GUL) policy, his tax-free death benefit would have been $1,266,620 or $1,216,127, respectively.

Sue will have $2,116,210 of tax-free death benefit through age 100, despite paying $250,000 in cumulative premiums (highlighted in blue in the chart below). Had Sue paid the same premiums for a Guaranteed Indexed Universal Life Insurance (GIUL) policy or a Guaranteed Universal Life Insurance (GUL) policy, her tax-free death benefit would have been $1,500,540 or $1,472,151, respectively.

Click to Enlarge

Action Steps – Customize Your Indexed Universal Life (IUL) Insurance Policy for Your Goals

Before purchasing an IUL insurance policy evaluate its: death benefit, underlying index, cap rate, participation rate, spread rate, bonuses, cost of insurance, charges, and cash flow capabilities in the form of policy withdrawals and loans. Work closely with an experienced financial professional to customize your IUL insurance policy for your goals.

Aaron Skloff, Accredited Investment Fiduciary (AIF), Chartered Financial Analyst (CFA), Master of Business Administration (MBA) is CEO of Skloff Financial Group, a Registered Investment Advisory firm specializing in financial planning, investment management and benefits for small to middle sized companies. He can be contacted at www.skloff.com or 908-464-3060.

![]()

Click Here for Your Life Insurance Quotes