Does Your State Tax Withdrawals from Pre-Tax Retirement Accounts? – Part 3

Money Matters – Skloff Financial Group Question of the Month – August 1, 2025

By Aaron Skloff, AIF, CFA, MBA

Q: We read ‘Pre-tax Versus Roth Employer Contributions to Retirement Accounts – Which Is Better?’ Part 1 and Part 2 and ‘Does Your State Tax Pre-Tax Contributions to Retirement Accounts?’ Part 1 and Part 2. and ‘Does Your State Tax Withdrawals from Pre-Tax Retirement Accounts?’ Part 1 and Part 2. Can you provide examples of the taxation on pre-tax contributions and withdrawals?

The Problem – Assuming Ben Franklin Was Right When He Claimed Nothing Is Certain Except Death and Taxes

Without proper planning, Ben Franklin was right about taxes. With proper planning, Ben Franklin was wrong about taxes.

The Solution – Proving Ben Franklin Was Wrong About Taxes with Proper Tax Planning – Avoid Unnecessary State Income Taxes Today and in the Future

With proper planning, you can make pre-tax contributions in states that defer income taxes and make withdrawals in states with low or no states income tax – a form of legal tax arbitrage. Let’s examine tax planning strategies below.

Are You Interested in Learning More?

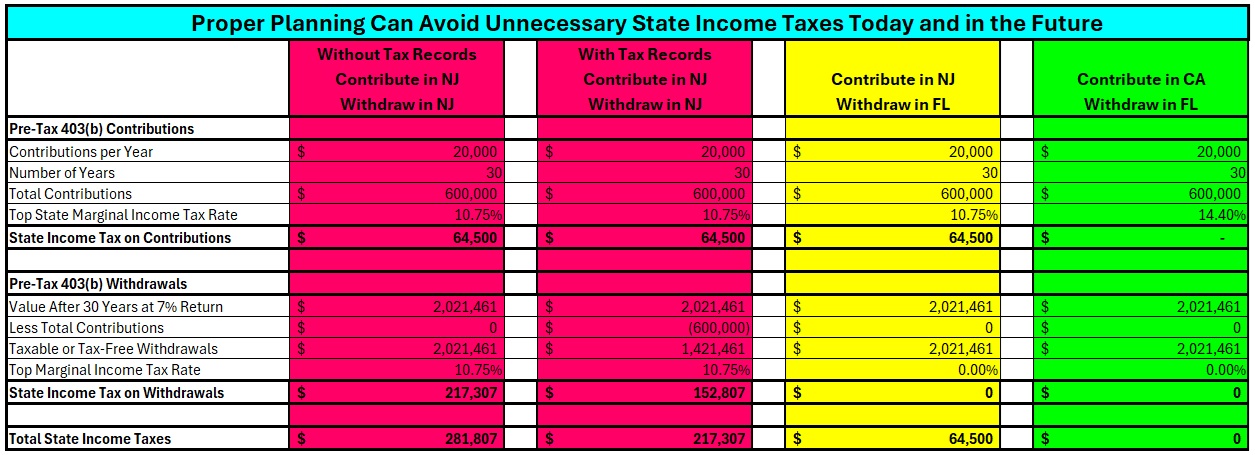

Pay 10.75% State Income Tax on Contributions and 10.75% on Withdrawals. New Jersey (NJ) taxes pre-tax contributions to 403(b) accounts. If you contribute $20,000 per year for 30 years for a total of $600,000 in NJ, you could be subject to the top marginal income tax bracket (TMITB) of 10.75% – resulting in $64,500 in NJ state income taxes. If you generate a 7% return per year, your portfolio would have a $2,021,461 ending value. NJ requires you to keep tax records of your contributions to avoid double taxation of your contributions upon withdrawal.

Upon completing a worksheet (“Worksheet C – IRA Withdrawals”), you can calculate your excludable amount (the part of your withdrawal that is a contribution) of your withdrawals. If you do not report your excludable amount, your contributions will be taxed again upon withdrawal. Without tax records required to calculate your excludable amount and based on a 10.75% TMITB, including taxing your contributions again, you would pay $217,307 in NJ state income states if you withdraw your balance in NJ. In total, you would pay $281,807 ($64,500 + $217,307) in NJ state income taxes. See the first red (highest danger zone) section of the table below.

Pay 10.75% State Income Tax on Contributions and 10.75% on Withdrawals. Let’s examine the same scenario as above, but this time you have kept 30 years of tax records. With the tax records required to calculate your excludable amount of $600,000 and based on a 10.75% TMITB, you would pay $152,807 in NJ state income states if you withdraw your balance in NJ. In total, you would pay $217,307 ($64,500 + $152,807) in NJ state income taxes if you withdraw your balance in NJ. See the second red (high danger zone) section of the table below.

Pay 10.75% State Income Tax on Contributions and 0.0% on Withdrawals. Let’s examine the first scenario above, but this time you complete your withdrawals when you are a resident of a state without state income taxes, Florida (FL). Based on a 0.0% state income tax rate, you would pay $0 in FL state income taxes if you withdraw your balance in FL. In total, you would have paid $64,500 ($64,500 + $0) in NJ state income taxes and $0 in FL state income taxes. See the yellow (danger zone) section of the table below.

Pay 0.0% State Income Tax on Contributions and 0.0% on Withdrawals. California (CA) does not tax pre-tax contributions to 403(b) accounts. If you contribute $20,000 per year for 30 years for a total of $600,000 in CA, you would not be subject to the top marginal income tax bracket (TMITB) of 14.4%. If you generate a 7% return per year, your portfolio would have a $2,021,461 value. If you complete your withdrawals when you are a resident of a state without a state income taxes, such as FL, you would pay $0 in FL state income taxes. In total, you would have paid $0 in CA state income taxes and $0 in FL state income taxes. See the green (safe zone) section of the table below.

Click to Enlarge

Action Steps

Work closely with your Registered Investment Adviser (RIA) to optimize your taxes, and pay the lowest tax rates in the current tax year and future tax years.

Aaron Skloff, Accredited Investment Fiduciary (AIF), Chartered Financial Analyst (CFA), Master of Business Administration (MBA) is CEO of Skloff Financial Group, a Registered Investment Advisory firm specializing in financial planning, investment management and benefits for small to middle sized companies. He can be contacted at www.skloff.com or 908-464-3060.

![]()

Are You Interested in Learning More?