Mega Backdoor Roth Examples

Skloff Financial Group Question of the Month – July 1, 2026

By Aaron Skloff, AIF, CFA, MBA

Q: We read ‘How to Complete a Backdoor Roth IRA’ and ‘How to Complete a Mega Backdoor Roth’. Can you give examples of the Mega Backdoor Roth?

The Problem — A Mega Backdoor Roth Can Be Botched

Making a cake is easy – just follow the recipe. Completing a Mega Backdoor Roth is easy – just follow the steps. While both are easy, both can be botched if completed incorrectly.

The Solution — Following Clear Examples of the Mega Backdoor Roth to Avoid Botching the Process

Internal Revenue Code (IRC) Sections 402(g) and 415(c) set deferral and total contribution limits. Think of them like the size of the baking pan and the size of the oven, respectively. They place controls around the process. Many payroll providers and/or 401(k) recordkeepers will cap contributions based on the IRC limits. High income earners are subject to Roth catch-up contributions, according to the SECURE 2.0 Act. Let’s look at two examples of the Mega Backdoor Roth based on the IRC limits.

Are You Interested in Learning More?

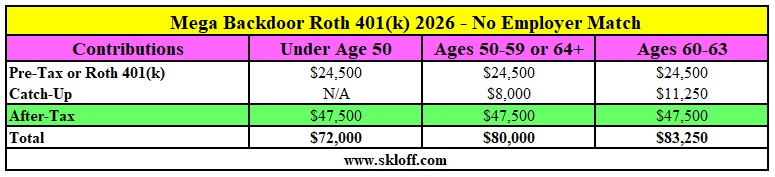

No Employer Match. A 401(k) participant who is under the age of 50 can contribute up to $24,500 on a pre-tax or Roth basis and up to $47,500 on an after-tax basis before reaching their $72,000 limit. A 401(k) participant who is age 50-59 or 64+ can contribute up to $32,500 on a pre-tax or Roth basis and up to $47,500 on an after-tax basis before reaching their $80,000 limit. A 401(k) participant who is age 60-63 can contribute up to $35,750 on a pre-tax or Roth basis and up to $47,500 on an after-tax basis before reaching their $83,250 limit.

Remember to immediately convert your after-tax contributions [ideally, automate this] to Roths inside the 401(k) to avoid creating unnecessary taxable withdrawals on the growth of after-tax contributions – creating a Mega Backdoor Roth.

Click to Enlarge

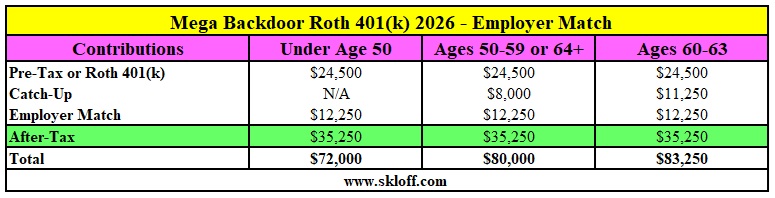

Employer Match. The following scenarios are based on the employer matching 50% of the base employee deferral, which excludes matching catch-up contributions. A 401(k) participant who is under the age of 50 can contribute up to $24,500 on a pre-tax or Roth basis. The employer can contribute a 50% match of $12,250. The participant can contribute up to $35,250 on an after-tax before reaching their $72,000 limit. A 401(k) participant who is age 50-59 or 64+ can contribute up to $32,500 on a pre-tax or Roth basis. The employer can contribute a 50% match of $12,250. The participant can contribute up to $35,250 on an after-tax basis before reaching their $80,000 limit. A 401(k) participant who is age 60-63 can contribute up to $35,750 on a pre-tax or Roth basis. The employer can contribute a 50% match of $12,250. The participant can contribute up to $35,250 on an after-tax basis before reaching their $83,250 limit.

Remember to immediately convert your after-tax contributions [ideally, automate this] to Roths inside the 401(k) to avoid creating unnecessary taxable withdrawals on the growth of after-tax contributions – creating a Mega Backdoor Roth.

Click to Enlarge

Action Step — Complete a Mega Backdoor Roth

Work closely with your Registered Investment Adviser to evaluate your Mega Backdoor Roth opportunities.

Aaron Skloff, Accredited Investment Fiduciary (AIF), Chartered Financial Analyst (CFA), Master of Business Administration (MBA) is CEO of Skloff Financial Group, a Registered Investment Advisory firm specializing in financial planning, investment management and benefits for small to middle sized companies. He can be contacted at www.skloff.com or 908-464-3060.

![]()

Have Your 401(k), 403(b), 457(b) Account Professionally Managed

Frequently Asked Questions

Q: What is a Mega Backdoor Roth, and why does it matter for high earners?

A Mega Backdoor Roth is a strategy that lets 401(k) participants contribute well beyond the standard elective deferral limit by making after-tax contributions to their plan and then converting those dollars to Roth — either inside the 401(k) or via rollover to a Roth IRA. It matters for high earners because standard pre-tax/Roth deferral limits cap out relatively quickly, while the combined limit under IRC Section 415(c) is much higher, leaving substantial room for additional after-tax savings that can ultimately grow and be withdrawn tax-free.

Q: What IRS rules govern how much can go into a Mega Backdoor Roth?

Two Internal Revenue Code sections set the boundaries: Section 402(g) caps the pre-tax/Roth elective deferral amount, and Section 415(c) caps total contributions from all sources — employee deferrals, after-tax contributions, and any employer match — combined. The article compares these to the size of a baking pan and the size of the oven: 402(g) controls how much goes into the “pan” as deferrals, while 415(c) controls the total that can fit in the “oven” across all contribution types, and many payroll providers or recordkeepers will automatically stop contributions once either limit is reached.

Q: How does the Mega Backdoor Roth work for someone with no employer match?

Without an employer match, the full gap between the elective deferral limit and the total 415(c) limit is available for after-tax contributions. For example, a participant under age 50 can contribute up to $24,500 pre-tax or Roth, then add up to $47,500 in after-tax contributions to reach the $72,000 total limit; participants age 50-59 or 64+ can contribute up to $32,500 pre-tax/Roth plus $47,500 after-tax to reach $80,000; and those age 60-63 can contribute up to $35,750 pre-tax/Roth plus $47,500 after-tax to reach $83,250.

Q: How does an employer match change the numbers?

When an employer match is involved, it counts toward the same 415(c) total limit, which reduces the room left for after-tax contributions. Using an example of a 50% match on base employee deferrals (excluding catch-up contributions), a participant under 50 who defers $24,500 pre-tax/Roth would receive a $12,250 match, leaving room for $35,250 in after-tax contributions to reach the $72,000 total — with similar adjustments of $35,250 in after-tax room for the 50-59/64+ and 60-63 age groups reaching their respective $80,000 and $83,250 totals.

Q: Why do age and catch-up contributions affect the limits?

Age-based catch-up contribution rules create different deferral and total limits for different age bands, which is why the examples break out participants under 50, ages 50-59 or 64+, and ages 60-63 separately. Under the SECURE 2.0 Act, high-income earners are also subject to special rules requiring their catch-up contributions to be made on a Roth basis rather than pre-tax, which is a detail that can affect how the deferral portion of the strategy is structured for higher earners in the catch-up-eligible age ranges.

Q: Why is it important to convert after-tax contributions to Roth quickly?

After-tax contributions, left unconverted, will generate investment growth that becomes taxable upon withdrawal — separate from the original contribution, which is already after-tax. By converting the after-tax dollars to Roth as soon as possible, ideally through an automated in-plan conversion feature, the growth on those dollars also becomes eligible for tax-free treatment, which is the step that actually turns an after-tax contribution into a true Mega Backdoor Roth rather than just a taxable after-tax account.

Q: What happens if the Mega Backdoor Roth is done incorrectly?

The article frames this with a baking analogy: making a cake or completing a Mega Backdoor Roth is straightforward if the steps are followed, but both can be “botched” if steps are skipped or done out of order — for instance, contributing beyond IRC limits, missing the conversion step, or failing to account for employer match dollars eating into available after-tax room. Following the specific numeric examples for one’s age band and match structure is presented as the way to avoid these errors.

Q: Does every 401(k) plan support the Mega Backdoor Roth?

The article doesn’t state that every plan supports it; it notes that many payroll providers and recordkeepers cap contributions based on IRC limits, which implies the mechanics depend on plan design — specifically, whether the plan allows after-tax (non-Roth) contributions and in-plan Roth conversions. The recommended action step is to work with a Registered Investment Adviser to evaluate whether a specific plan supports the opportunity.