Professionally Managed 401(k) Account Rollovers Can Generate 3% to 4% Higher Returns Per Year

Money Matters – Skloff Financial Group Question of the Month – January 1, 2026

By Aaron Skloff, AIF, CFA, MBA

Q: I recently left my company. My spouse is still working for her company. What are the advantages of rolling over our 401(k) accounts into professionally managed IRAs?

The Problem – Getting Professional Advice to Optimize Return and Risk in Your 401(k) Account

Charles Schwab’s ‘2024 401(k) Participant Study’ found 61% of retirement savers believe their financial situation warrants professional advice, compared with 55% in 2023. Even disciplined, experienced investors can end up with inappropriate risk levels and mediocre returns in their 401(k) accounts. Many are constrained by limited investment options and target date funds inconsistent with their needs.

The Solution – Professional Managed 401(k) Accounts and IRAs Can Generate 3% to 4% Higher Returns Net of Fees Per Year

Once you leave your company, you can complete a tax-free rollover of your 401(k) account to a professionally managed IRA account, regardless of your age. Many companies allow you to complete a tax-free in-service rollover of your 401(k) account to a professionally managed IRA once you reach age 59 ½, even if you are still working for your company. Professionally managed IRAs offer virtually unlimited investment options, which can be optimized to meet your needs.

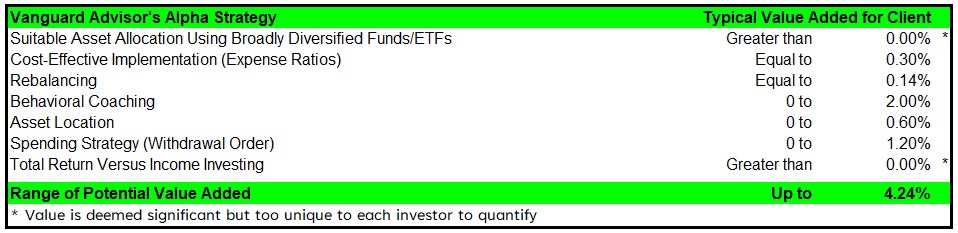

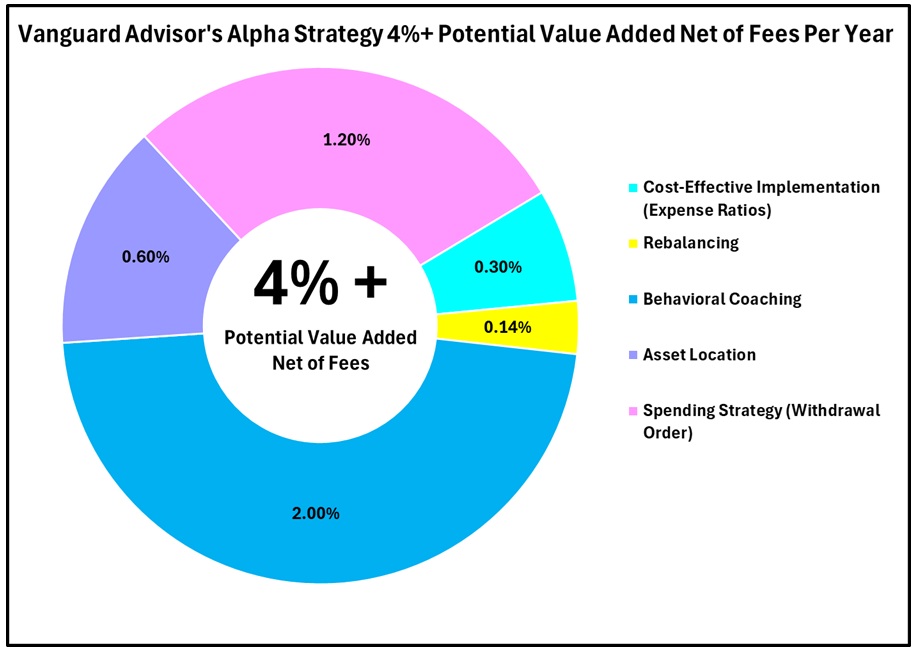

Vanguard’s 2022 ‘Putting a Value on Your Value: Quantifying Vanguard Advisor’s Alpha’ study concluded that professionally managed accounts can add 3% to 4% higher returns net of fees per year.

The Vanguard study attributed the higher performance to the following components. See the table and chart below.

Click to Enlarge

Rollover Your 401(k), 403(b), 457(b) Account to a Professionally Managed IRA

As seen in the table above, Suitable Asset Allocation is deemed significant. According to Vanguard, “a whopping 88% of your experience (the volatility you encounter and the returns you earn) can be traced back to your asset allocation”.

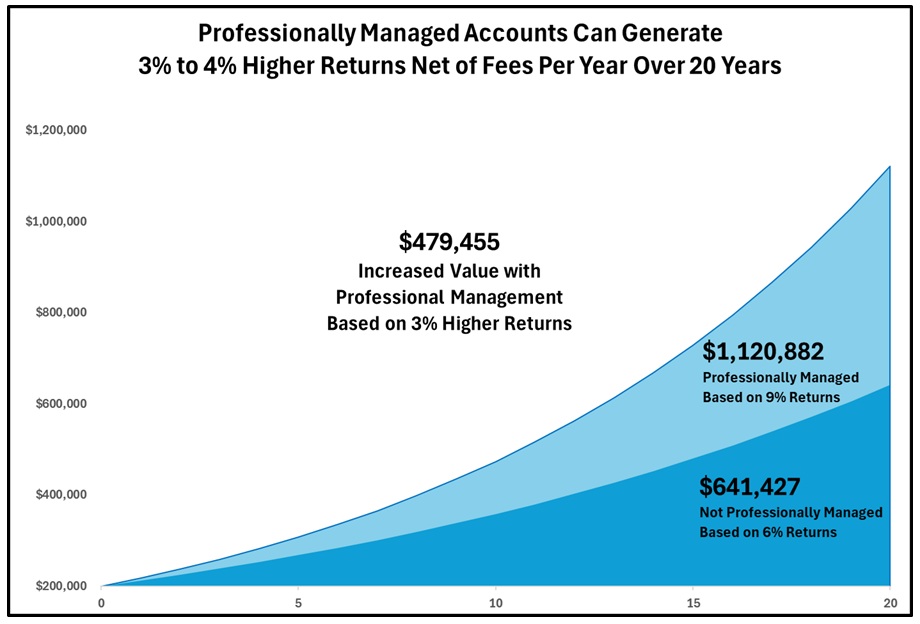

Professionally Managed Accounts Can Generate 75% Higher Values Over 20 Years. Applying Vanguard’s study, 3% higher returns per year can generate a 75% higher account value over 20 years. Let’s look at an example of a $200,000 401(k) account that is not professionally managed, based on 6% annual returns. Over 20 years, the account that is not professionally managed grows to $641,427. Let’s look at an example of a $200,000 IRA that is professionally managed, based on 9% annual returns net of fees. Over 20 years, the professionally managed account grows to $1,120,882. The professionally managed account has a $479,455 higher value, equating to a 75% higher value. See the chart below.

Click to Enlarge

Click to Enlarge

Action Steps

Rollover your 401(k) accounts from former employers to a professionally managed IRA. Complete in-service rollovers once you reach age 59 ½ to a professionally managed IRA. A professionally managed IRA can generate 3% to 4% higher returns net of fees per year, resulting in a 75% higher account value over 20 years. Work closely with your Registered Investment Adviser (RIA) to professionally manage your accounts.

Aaron Skloff, Accredited Investment Fiduciary (AIF), Chartered Financial Analyst (CFA), Master of Business Administration (MBA) is CEO of Skloff Financial Group, a Registered Investment Advisory firm specializing in financial planning, investment management and benefits for small to middle sized companies. He can be contacted at www.skloff.com or 908-464-3060.

![]()

Rollover Your 401(k), 403(b), 457(b) Account to a Professionally Managed IRA

Frequently Asked Questions

Q: What are the benefits of rolling over my old 401(k) to a professionally managed IRA?

Rolling over a former employer’s 401(k) into a professionally managed IRA can provide access to a much broader range of investment choices than most employer-sponsored plans. Instead of being limited to a short list of mutual funds or target-date funds, investors can build customized portfolios using ETFs, individual securities, bonds, and alternative investment strategies tailored to their goals, risk tolerance, and tax situation. Professional management can also provide ongoing portfolio monitoring, rebalancing, tax-efficient investment decisions, and retirement income planning that may improve long-term outcomes. According to Vanguard’s Advisor’s Alpha research, professional advice can potentially add approximately 3% to 4% in net annual value through disciplined investment and behavioral strategies.

Q: Can professionally managed accounts really generate 3% to 4% higher annual returns?

The additional value is not simply the result of selecting better-performing investments. Vanguard’s research attributes the potential 3% to 4% annual improvement to several factors working together, including appropriate asset allocation, systematic portfolio rebalancing, minimizing behavioral mistakes during market volatility, tax-efficient investing, and disciplined withdrawal strategies during retirement. While no adviser or investment strategy can guarantee higher returns, these value-added services have historically improved investor outcomes by helping clients remain invested, control risk, and make more informed financial decisions over time. Actual results will vary depending on market conditions and investor behavior.

Q: Should I always roll my old 401(k) into an IRA after leaving my employer?

Not necessarily. A rollover is often beneficial because it can simplify retirement accounts and expand investment flexibility, but it is not automatically the best choice for everyone. Some employer plans offer exceptionally low institutional investment costs, valuable stable value funds, strong creditor protection, or special withdrawal rules for employees who retire after age 55. Before initiating a rollover, compare investment options, fees, services, withdrawal flexibility, and tax considerations. A fiduciary financial adviser can help determine whether keeping assets in the employer plan or completing a rollover better aligns with your retirement objectives.

Q: Can I roll over my 401(k) while I’m still working?

In many cases, yes. Some employer-sponsored retirement plans allow what’s known as an “in-service rollover” or “in-service withdrawal,” typically once an employee reaches age 59½. This allows participants to transfer some or all of their vested 401(k) balance into an IRA without leaving their job, while continuing to contribute to the employer’s retirement plan and receive matching contributions if available. Because plan rules vary significantly, employees should verify whether their specific 401(k) permits in-service rollovers before making plans.

Q: How can I avoid taxes and penalties when completing a 401(k) rollover?

The safest approach is a direct trustee-to-trustee rollover, where the retirement funds move directly from the 401(k) plan to the IRA custodian without the money ever passing through your hands. This method avoids mandatory tax withholding and significantly reduces the risk of triggering income taxes or early withdrawal penalties. Indirect rollovers, where the participant receives the funds first, must generally be completed within 60 days and are subject to additional IRS rules that can create unintended tax consequences if deadlines are missed.

Q: What mistakes should investors avoid after completing a 401(k) rollover?

One of the biggest mistakes is allowing rollover proceeds to remain in cash instead of investing them according to a long-term strategy. Research has found that many investors inadvertently leave IRA rollover assets sitting in money market or settlement accounts for extended periods, potentially missing years of market growth. Other common mistakes include selecting an inappropriate asset allocation, failing to rebalance the portfolio, ignoring investment costs, and making emotional decisions during market volatility. Working with a professional investment adviser can help ensure rollover assets are promptly invested and managed according to a disciplined long-term financial plan.