Using an IRA or 401(k) to Pay for Hybrid-Combination Life and Long Term Care Insurance – Long Term Care University

Long Term Care University – Question of the Month – 10/15/19

By Aaron Skloff, AIF, CFA, MBA

Q: We read the Long Term Care University article that compares Traditional to Hybrid-Combination Life and Long Term Care (LTC) Insurance and prefer the Hybrid-Combination LTC policy. Can we pay for a Hybrid LTC policy with money from an IRA or 401(k)?

Overview. With Traditional LTC policies, premiums can be increased, and you may not receive any benefits if you do not need LTC. With Hybrid LTC policies the benefits and premiums are guaranteed. The insurance company either: 1) pays you if you need LTC, 2) pays your heirs if you do not need LTC, 3) pays you and your heirs if you need a modest amount of LTC or 4) pays you a refund if you cancel the policy.

Click Here for Your Long Term Care Insurance Quotes

The Problem – Paying for a Hybrid LTC Insurance Policy with Money Trapped in Pre-Tax Retirement Accounts

For many savers, their largest assets are pre-tax retirement accounts, like IRAs and 401(k)s. They have more than adequate retirement assets, but inadequate savings outside of their retirement accounts. They would like to make a single withdrawal from pre-tax retirement accounts, but withdrawals are taxed as income and could increase their tax bracket – generating a large tax bill. They could make periodic withdrawals, but coordinating withdrawals from retirement accounts and facilitating payments for a Hybrid LTC policy can be cumbersome.

The Solution – Using an IRA or 401(k) with Pre-Tax Dollars to Pay for a Hybrid Life LTC Insurance Policy

OneAmerica State Life Asset Care is a Hybrid LTC Insurance policy that can be funded with pre-tax retirement account dollars. State Life Insurance Company Group is part of OneAmerica, an A.M. Best A+ rated company, founded in 1877.

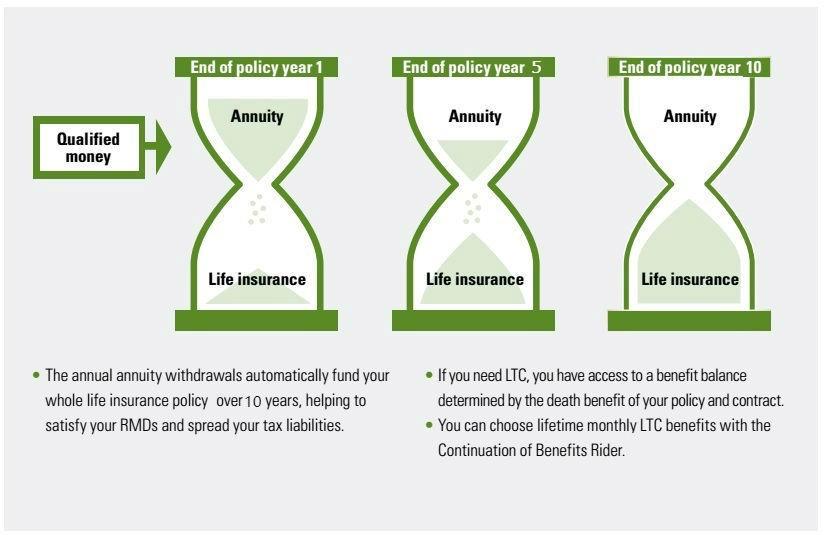

OneAmerica State Life Asset Care is Unique Because It Can be Paid with Pre-Tax Retirement Assets and Provides Lifetime Benefits. OneAmerica State Life Asset Care allows you to rollover a portion of your retirement account, such as an IRA or 401(k), to an IRA deferred annuity. Then, from that IRA annuity a withdrawal is taken annually to fund a 10-pay Hybrid LTC policy. These annual withdrawals defer taxes and still meet your Required Minimum Distributions (RMDs). OneAmerica State Life seamlessly facilitates the payments and RMDs. Asset Care can insure you and your partner using just one of your retirement accounts. You can also purchase a Lifetime benefit rider.

Click to Enlarge

One of the largest long term care insurance companies reported that 50% of all claims dollars it has paid are due to dementia, including Alzheimer’s disease. According to the Alzheimer’s Association, 1 in 9 people ages 65 and older and about 1 in 3 people ages 85 and older have Alzheimer’s disease. The duration of Alzheimer’s disease is generally 4-8 years after a diagnosis, but can last as long as 20 years. Most companies mitigate their risks and increase consumers’ risks by limiting coverage to a maximum of 6 or 7 years of care. OneAmerica State Life Asset Care offers lifetime benefits with an unlimited number of years of care and an unlimited dollar amount of LTC benefits.

OneAmerica State Life Asset Care Policy Options for Singles or Partners. The policy options include: Benefit periods of 25 months to lifetime (unlimited number of years); Inflation protection of none or 3% compound or 5% compound; Elimination period of 0 days and 90 days; Surrender value (refund if cancelled); Use of qualified funds (pre-tax retirement accounts: 401(k) and IRA) ; Second to die death benefit.

Numbers Speak Louder than Words. Let’s look at a husband and wife, Bill and Sue, who are each 60 years old and reside in New Jersey. Bill waits until he is 60 years old to buy his policy that covers both he and Sue. If purchased before age 59 ½, Bill could be subject to tax penalties. Bill transfers $200,000 from his pre-tax Traditional IRA on a tax-free basis. With this one-time premium payment, they immediately gain a $7,185 per month, per person LTC benefit available for an unlimited number of months for LTC costs; literally a lifetime worth of LTC. They also gain a $239,497 death benefit by year 9 (higher in earlier years) when the second person dies, if the policy’s LTC benefits are unused. Please see the chart below.

Alternatively, Bill transfers $200,000 from his pre-tax Traditional IRA on a tax-free basis. With this one-time premium payment, they immediately gain a $3,579 per month, per person LTC benefit available with 3% compound inflation protection for an unlimited number of months for LTC costs; literally a lifetime worth of LTC. In 20 years, when they are 80 years old and likely to need care, they would have a $6,277 per month, per person LTC benefit available for an unlimited number of months for LTC costs. They also gain a $119,314 death benefit by year 9 (higher in earlier years) when the second person dies, if the policy’s LTC benefits are unused. Please see the chart below.

Click to Enlarge

Action Steps and Conclusions. OneAmerica State Life Asset Care provides lifetime benefits LTC benefits and can be funded with pre-tax retirement accounts. Since premiums vary greatly based on age, health and marital status, request individualized quotes.

Aaron Skloff, Accredited Investment Fiduciary (AIF), Chartered Financial Analyst (CFA) charter holder, Master of Business Administration (MBA), is the Chief Executive Officer of Skloff Financial Group, a Registered Investment Advisory firm. The firm specializes in financial planning and investment management services for high net worth individuals and benefits for small to middle sized companies. He can be contacted at www.skloff.com or 908-464-3060.

![]()