Hybrid Annuity and Long Term Care – Long Term Care University

Long Term Care University – Question of the Month – 06/15/26

By Aaron Skloff, AIF, CFA, MBA

Q: We read the Long Term Care University article ‘Traditional Versus Hybrid Life and Long Term Care Insurance’ and ‘1035 Tax-Free Exchange‘. Can you please explain Hybrid Annuities with Long Term Care (LTC)?

The Problem – Paying for a Long Term Care with a Traditional Annuity Can be Taxing

According to the U.S. Department of Health and Human Services, 7 in 10 people over the age of 65 will require long term care (LTC). According to a Gallop survey, 73% of annuity owners intend to use their annuity as an emergency fund for a catastrophic illness or nursing home care. Unfortunately, withdrawals of gains from traditional annuities are taxed as income. Based on a 25% federal income tax rate (excluding state income taxes), withdrawing $100,000 of gains would cost you $25,000 in taxes.

Click Here for Your Long Term Care Insurance Quotes

The Solution – Hybrid Annuity and Long Term Care Policies that Pay Tax-Free Long Term Care Benefits

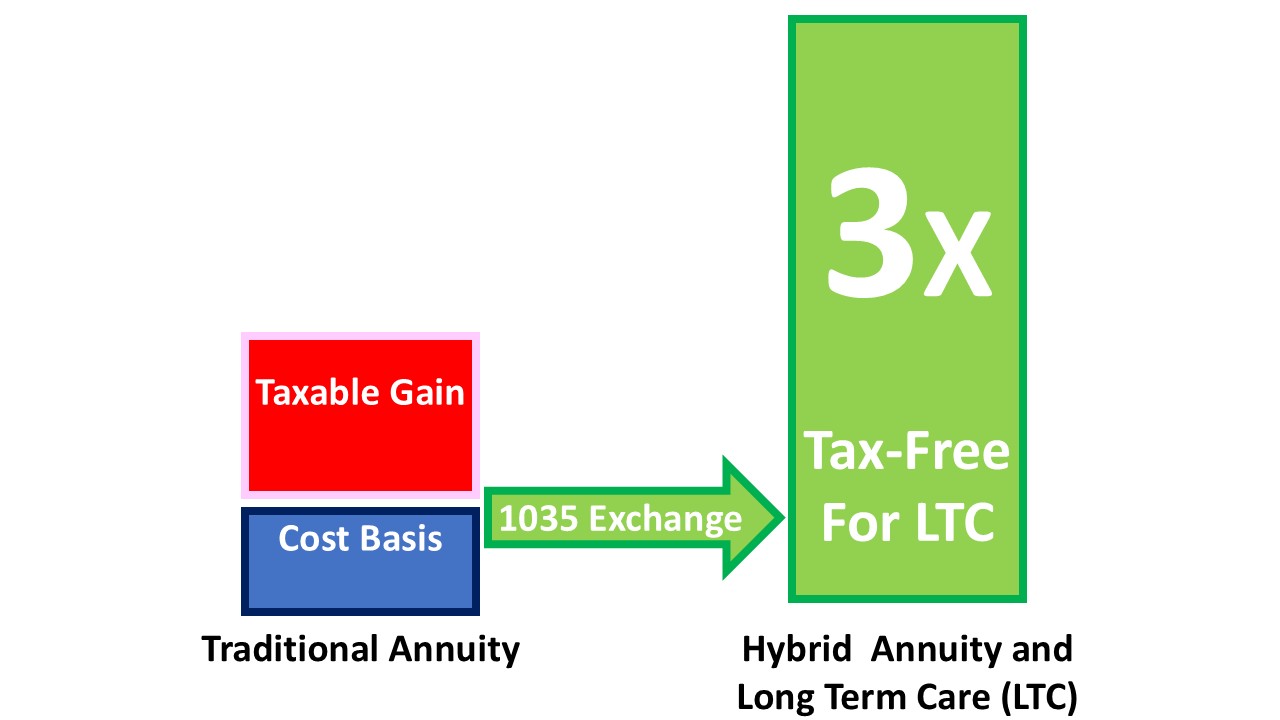

Many consumers purchase an annuity based on their existing and future needs. As those needs change, they realize their existing annuity is inadequate. With the exchange of an old traditional annuity to a new Hybrid Annuity and LTC, you can gain double, triple or even unlimited value of the original annuity for LTC costs. The Pension Protection Act (PPA) of 2006 added additional flexibility to the tax-free 1035 exchange of old annuities to new annuities. If the new annuity is a Hybrid Annuity and LTC policy and withdrawals are for LTC costs, all the gains from the original policy and the doubling, tripling, etc. of value are tax-free.

Numbers Speak Louder Than Words. Let’s look at examples for Bill (70) and Sue (70). They can each purchase an individual policy for $100,000 and each receive $311,485 of tax-free long term care benefits – over three times the purchase price. They can purchase a shared (joint policy) for $200,000 and receive $623,371 of combined tax-free long term care benefits – over three times the purchase price.

Exchanging an Existing Traditional Annuity into a Hybrid Annuity and Long Term Care. If they already own annuities, they will receive the same benefits based on the same purchase price and gain the benefit of exchanging a future taxable event into tax-free long term care benefits. See the images below.

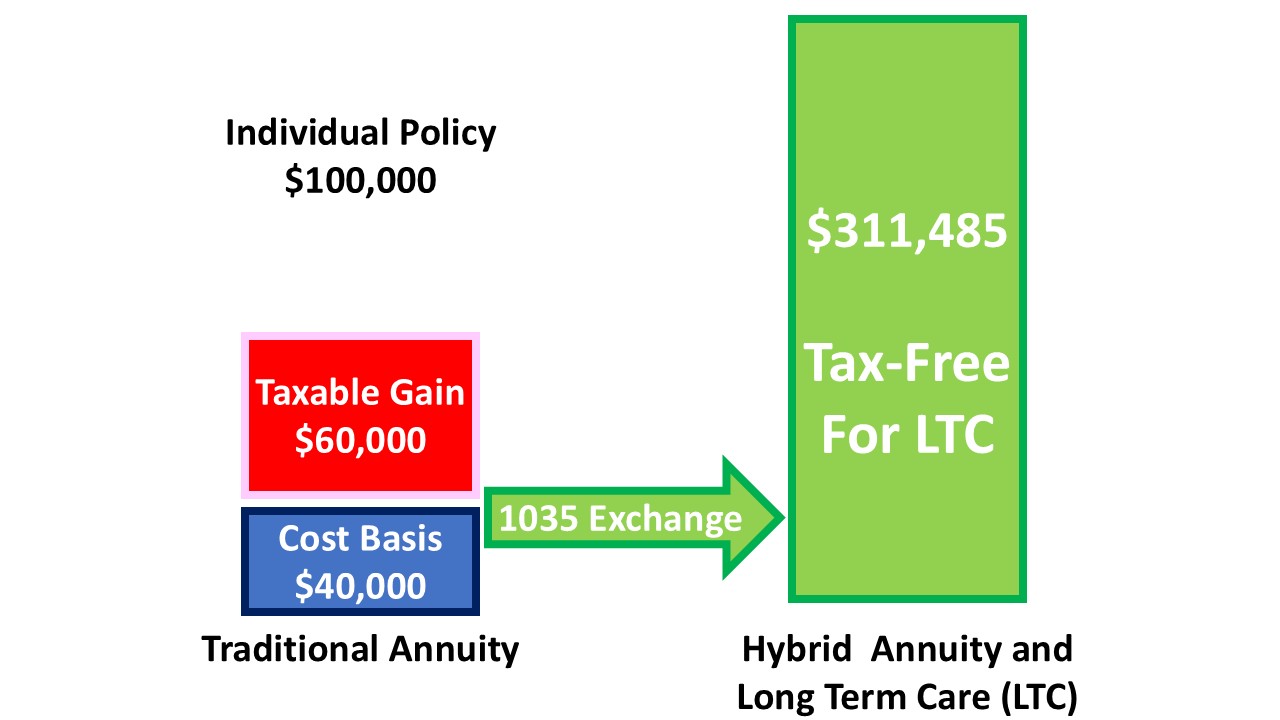

Bill has his own traditional annuity. Sue has her own traditional annuity. While they paid $40,000 for each for their individual policies, the annuities have $60,000 of taxable gain and are each now valued at $100,000. Each of their $100,000 policies can be exchanged into their own Hybrid Annuity and LTC policy that will each provide $311,485 of tax-free long term care benefits. See the images below.

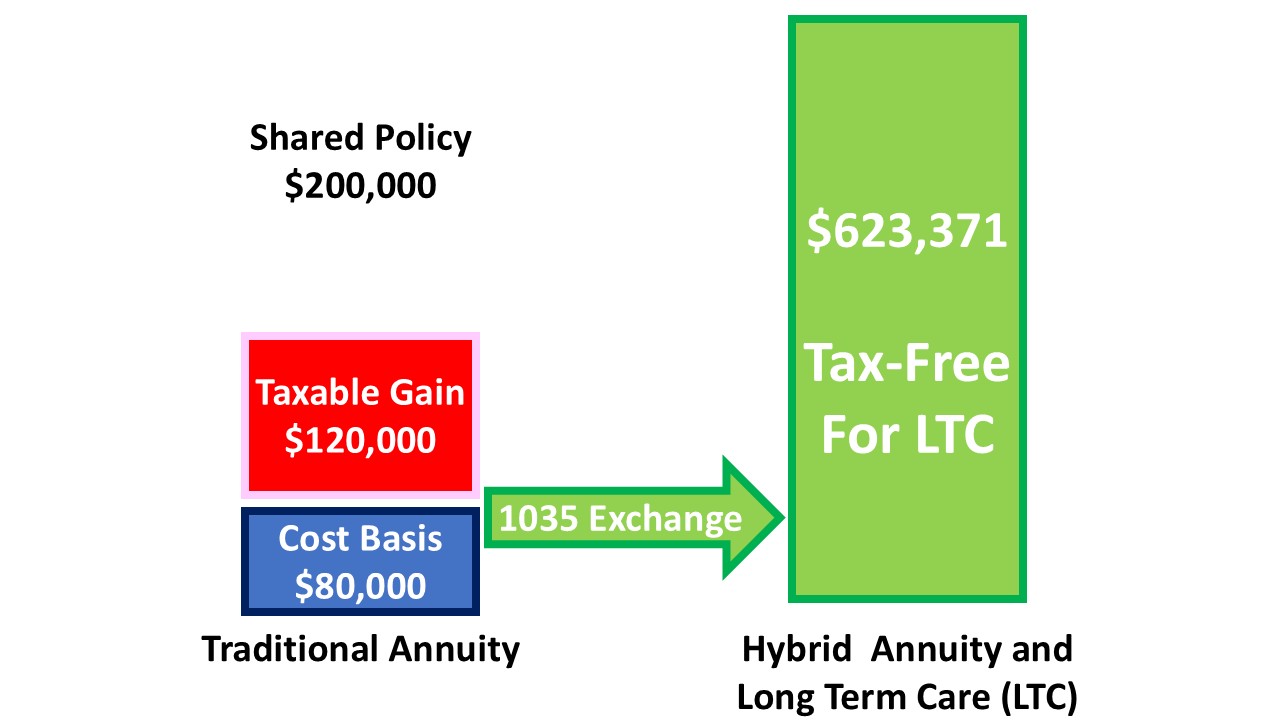

They also own a shared (joint) traditional annuity. While they paid $80,000 for the joint traditional annuity, it has a $120,000 taxable gain and is now valued at $200,000. Their joint $200,000 policy can be exchanged into a shared (joint) Hybrid Annuity and LTC policy that will provide $623,371 of combined tax-free long term care benefits. See the images below.

Click to Enlarge

Click to Enlarge

Click to Enlarge

Conclusions. A Hybrid Annuity and Long Term Care policy triples your value in tax-free LTC benefits, whether you fund it with a new purchase or a tax-free 1035 exchange. Since premiums vary greatly based on age, health and marital status, request individualized quotes.

Aaron Skloff, Accredited Investment Fiduciary (AIF), Chartered Financial Analyst (CFA) charter holder, Master of Business Administration (MBA), is the Chief Executive Officer of Skloff Financial Group, a Registered Investment Advisory firm. The firm specializes in financial planning and investment management services for high net worth individuals and benefits for small to middle sized companies. He can be contacted at www.skloff.com or 908-464-3060.

![]()

Click Here for Your Long Term Care Insurance Quotes

Frequently Asked Questions

Q: Why can paying for long-term care with a traditional annuity create a tax problem?

Because withdrawals of the gains inside a traditional annuity are taxed as ordinary income, using that money for long-term care can come with a real tax bill. For example, withdrawing $100,000 of gains at a 25% federal income tax rate would cost $25,000 in taxes, before even factoring in state income taxes.

Q: What is a Hybrid Annuity and Long Term Care policy?

It’s a policy created by exchanging an old traditional annuity for a new annuity that combines long-term care benefits, allowing the original policy’s value to be used for LTC costs at double, triple, or even unlimited value compared to the original annuity.

Q: How does the exchange from a traditional annuity to a Hybrid Annuity and LTC policy avoid taxes?

The Pension Protection Act (PPA) of 2006 expanded the tax-free 1035 exchange rules so that annuities can be exchanged tax-free into a Hybrid Annuity and LTC policy; as long as withdrawals from the new policy are used for LTC costs, both the original gains and the added multiplied value come out completely tax-free.

Q: How many people are likely to need long-term care, and how do annuity owners plan to use their annuities for it?

According to the U.S. Department of Health and Human Services, 7 in 10 people over age 65 will require long-term care, and a Gallup survey found that 73% of annuity owners already intend to use their annuity as an emergency fund for a catastrophic illness or nursing home stay.

Q: How much can an individual gain in tax-free LTC benefits through this strategy?

Using the example in the article, a 70-year-old purchasing an individual policy for $100,000 could receive $311,485 of tax-free long-term care benefits — over three times the purchase price.

Q: How does this work for couples with a joint policy?

A couple purchasing a shared (joint) policy for $200,000 could receive $623,371 of combined tax-free long-term care benefits, also more than three times the purchase price, according to the article’s example.

Q: What happens if a couple already owns individual traditional annuities with taxable gains?

Using Bill and Sue’s example, each paid $40,000 for their own annuity, which grew to $100,000 with $60,000 of taxable gain; by exchanging each $100,000 policy into its own Hybrid Annuity and LTC policy, each would receive $311,485 in tax-free long-term care benefits instead of facing a future taxable withdrawal.

Q: What happens if a couple owns a joint traditional annuity instead?

In the article’s example, Bill and Sue paid $80,000 for a joint traditional annuity that grew to $200,000 with a $120,000 taxable gain; exchanging that joint policy into a shared Hybrid Annuity and LTC policy would provide $623,371 of combined tax-free long-term care benefits.

Q: Do premiums for these policies vary from person to person?

Yes — the article notes that premiums vary greatly based on age, health, and marital status, which is why individualized quotes are recommended before deciding on a policy.

Q: What’s the main takeaway of this strategy?

Whether funded through a new purchase or a tax-free 1035 exchange of an existing annuity, a Hybrid Annuity and Long Term Care policy can roughly triple the value available for tax-free long-term care benefits compared to the original annuity amount.