Income Tax and Capital Gains Rates 2025 – Part 2

Money Matters – Skloff Financial Group Question of the Month – April 1, 2025

By Aaron Skloff, AIF, CFA, MBA

Q: We read ‘Income Tax and Capital Gains Rates 2025’ Part 1. Can you give examples of marginal and effective income tax rates?

The Problem – Maze of Marginal and Effective Income Tax Rates

Looking at an income tax rates table may lead some to belief all their income is taxed at the top marginal income tax bracket.

Are You Interested in Learning More?

The Solution – A Side-by-Side Comparison of Marginal and Effective Income Tax Rates

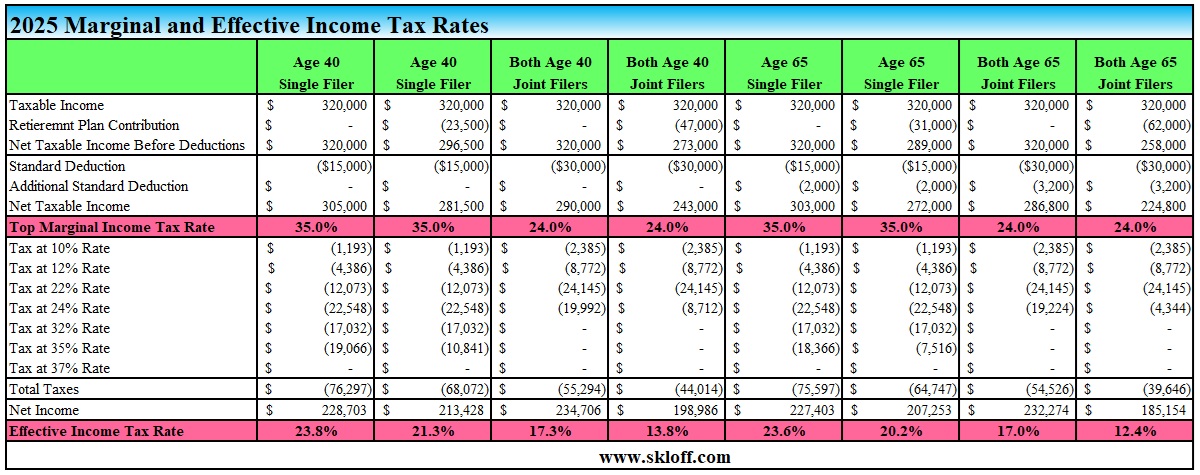

By examining scenarios on a side-by-side basis, we can see how age, adjustments to income, standard deductions and filing status can affect income taxes. The 2025 standard deduction for single filers under age 65 is $15,000, with an additional $2,000 for those 65 and over. The 2025 standard deduction for joint filers under age 65 is $30,000, with an additional $3,200 for those 65 and over. The 2025 maximum pre-tax contribution limit to many employer retirement plans (i.e.: 401(k), 403(b) and 457(b)) is $23,500 for those under age 50, $31,000 for those 50-59 or 64+, and $34,750 for those 60-63. The following scenarios are based on taking the standard deduction.

Age 40 Single Filer Not Contributing Versus Maximizing Contributions to a Retirement Plan. A 40-year-old single filer with $320,000 of income would be subject to a 35% top marginal income tax bracket. If he does not contribute to his employer retirement plan, he will pay $76,297 in taxes and have a 23.8% effective income tax rate. If he maximizes contributions to his employer retirement plan, he will pay $68,072 in taxes and have a 21.3% effective income tax rate.

Both Age 40 Joint Filers Not Contributing Versus Maximizing Contributions to a Retirement Plan. Two 40-year-old joint filers with $320,000 of combined income would be subject to a 24% top marginal income tax bracket. If they do not contribute to their company retirement plan, they will pay $55,294 in taxes and have a 17.3% effective income tax rate. If they maximize contributions to their employer retirement plan, they will pay $44,014 in taxes and have a 13.8% effective income tax rate.

Age 65 Single Filer Not Contributing Versus Maximizing Contributions to a Retirement Plan. A 65-year-old single filer with $320,000 of income would be subject to a 35% top marginal income tax bracket. If he does not contribute to his employer retirement plan, he will pay $75,597 in taxes and have a 23.6% effective income tax rate. If he maximizes contributions to his employer retirement plan, he will pay $64,747 in taxes and have a 20.2% effective income tax rate.

Both Age 65 Joint Filers Not Contributing Versus Maximizing Contributions to a Retirement Plan. Two 65-year-old joint filers with $320,000 of combined income would be subject to a 24% top marginal income tax bracket. If they do not contribute to their company retirement plan, they will pay $54,526 in taxes and have a 17.0% effective income tax rate. If they maximize contributions to their employer retirement plan, they will pay $39,646 in taxes and have a 12.4% effective income tax rate.

Click to Enlarge

Action Steps

Work closely with your Registered Investment Adviser (RIA) to optimize your marginal income tax brackets to pay the lowest effective income tax rates in the current tax year and future tax years.

Aaron Skloff, Accredited Investment Fiduciary (AIF), Chartered Financial Analyst (CFA), Master of Business Administration (MBA) is CEO of Skloff Financial Group, a Registered Investment Advisory firm. He can be contacted at www.skloff.com or 908-464-3060.

![]()

Are You Interested in Learning More?