Securian Minnesota Life SecureCare IV Hybrid Life and Long Term Care Insurance Review – Long Term Care University

Long Term Care University – Question of the Month – 04/15/26

By Aaron Skloff, AIF, CFA, MBA

Q: We read the Long Term Care University article ‘Traditional Versus Hybrid Life and Long Term Care Insurance’ and prefer the Hybrid Long Term Care Insurance (LTC) policy. Can you please review the Securian Minnesota Life SecureCare IV Hybrid LTC policy?

Overview.Minnesota Life is part of Securian Financial Group, an A.M. Best A+ rated, founded in 1880. The Securian Minnesota Life SecureCare policy is a Hybrid Life and Long Term Care Insurance (also called Combination or asset based) policy. With Traditional LTC policies, premiums can be increased and you may not receive any benefits if you do not need LTC. With Hybrid LTC policies the benefits and premiums are guaranteed. The insurance company either: 1) pays you if you need LTC, 2) pays your heirs if you do not need LTC, 3) pays you and your heirs if you need a modest amount of LTC or 4) pays you a refund if you cancel the policy.

Click Here for Your Long Term Care Insurance Quotes

Securian Minnesota Life SecureCare IV is Unique Because it is a Cash Indemnity Policy. There are two primary benefit payment methods among LTC policies. Reimbursement policies, the most common, require you to submit documentation of all expenses for reimbursement up to your monthly LTC benefits. Cash Indemnity policies pay up to your monthly LTC benefits, regardless of your expenses.

Securian Minnesota Life SecureCare IV is Unique Because It Pays for Formal and Informal Care from Family and Friends. Most LTC policies prohibit informal care, particularly if the care is provided by a family member. The Securian Minnesota Life SecureCare IV policy allows you to use formal care providers (home care agencies or facilities) and informal care providers, including family and friends. Since informal care providers can be much less costly, you can obtain significantly more care with a lower monthly benefit. This is very valuable for home care.

Securian Minnesota Life SecureCare IV Policy Options. The policy options include: Benefit periods of 4-8 years; Inflation protection of none, 3% simple, 3% compound, 5% simple and 5% compound; Elimination period of 90 days, with 0 day retroactive; Residual life insurance benefit (even if you deplete all of your LTC benefits) equal to the lesser of 10% of the face amount of insurance or $10,000. International Benefits are 100% of monthly maximum LTC benefits for the entire benefit period (e.g.: 6 years).

Securian Minnesota Life SecureCare IV Policy Premium Payment Options. They include: one time (single-pay), 5 years (5-pay), 7 years (7-pay), 10 years (10-pay), 15 Years (15-pay) and 20 Years (20-pay) based on age. Like buying a home, the longer your payment option, the higher your cumulative payments.

Securian Minnesota Life SecureCare IV Tax Benefits. In addition to the LTC and death benefits being paid on a tax free basis, the LTC portion of the premium is eligible for a tax deduction by individuals or can be expensed by businesses (including sole proprietorships). Individuals can pay from their HSA.

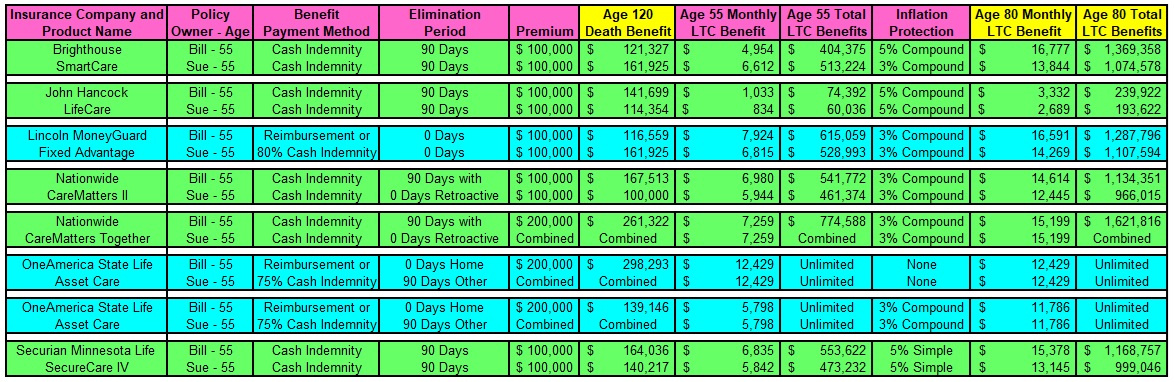

How Securian Minnesota Life SecureCare IV Compares with Other Hybrid LTC Policies. Let’s look at a husband and wife, Bill and Sue, who are each 55 years old and reside in Maryland. They each pay a $100,000 one-time premium ($200,000 combined with Nationwide and State Life) and are expected to need LTC in 25 years at the age of 80. They are comparing Hybrid policies that offer the largest LTC benefits and inflation protection (unless noted otherwise) and prefer cash indemnity. See reimbursement policies in blue and cash indemnity policies in green in the chart below.

Securian Minnesota Life SecureCare IV Outperforms Competitors with High Monthly and Total LTC Benefits. Bill will have $15,378 monthly and $1,168,757 total LTC benefits, while Sue will have $13,145 and $999,046, respectively. Brighthouse SmartCare is a strong cash indemnity alternative for Bill and Sue due to its high monthly and total LTC benefits, and its option to link policy values to major market indices. John Hancock LifeCare is notable for its option to link policy values to major market indices. Lincoln MoneyGuard Fixed Advantage is a strong (partial cash indemnity) alternative Bill and Sue due to its high monthly LTC benefits to its 0 day elimination period. Nationwide Care Matters II is a strong cash indemnity alternative for Bill and Sue due to its high monthly and total LTC benefits and its 90 day with zero day retroactive elimination period. Nationwide CareMatters Together is a strong cash indemnity alternative for Bill and Sue due to its high monthly LTC benefits and its 90 day with zero day retroactive elimination period. OneAmerica State Life Asset Care is a strong (partial cash indemnity) alternative due to its unlimited, lifetime total LTC benefits.

Click to Enlarge

Conclusions. Securian Minnesota Life SecureCare IV provides high monthly and total LTC benefits, with the flexibility of formal and informal care providers (including family and friends). Since premiums vary greatly based on age, health and marital status, request individualized quotes.

Aaron Skloff, Accredited Investment Fiduciary (AIF), Chartered Financial Analyst (CFA) charter holder, Master of Business Administration (MBA), is the Chief Executive Officer of Skloff Financial Group, a Registered Investment Advisory firm. The firm specializes in financial planning and investment management services for high net worth individuals and benefits for small to middle sized companies. He can be contacted at www.skloff.com or 908-464-3060.

![]()

Click Here for Your Long Term Care Insurance Quotes

Frequently Asked Questions

Q: What is Securian Minnesota Life SecureCare IV, and how does it work?

Securian Minnesota Life SecureCare IV is a hybrid life insurance and long-term care (LTC) insurance policy that combines a guaranteed death benefit with tax-qualified long-term care benefits. If you need long-term care, the policy provides cash indemnity benefits that can be used however you choose—including paying family caregivers, home health aides, assisted living, or nursing home expenses—without submitting receipts. If you never need long-term care, your beneficiaries receive the remaining death benefit. The policy also includes guaranteed premiums, several premium payment options, optional inflation protection, and multiple return-of-premium choices, making it a flexible alternative to traditional standalone LTC insurance.

Q: How is SecureCare IV different from traditional long-term care insurance?

Unlike traditional long-term care insurance, which generally operates on a reimbursement basis and can be considered “use-it-or-lose-it,” SecureCare IV pays a monthly cash benefit directly to the policyholder once benefit eligibility is met. There are no receipts to submit or restrictions on how the money is spent, giving families greater flexibility during a stressful time. In addition, if long-term care is never needed, the policy still provides value through its life insurance death benefit or available return-of-premium options, helping reduce the concern that premiums could be paid for decades without receiving any benefits.

Q: Who is a good candidate for SecureCare IV?

SecureCare IV is often a good fit for individuals between ages 40 and 75 who want to protect retirement assets from long-term care expenses while ensuring their premium dollars provide value even if care is never needed. It may appeal to people who dislike the uncertainty of traditional LTC insurance, want guaranteed premiums and benefits, or wish to leave a legacy to heirs if long-term care is never required. The policy is particularly attractive for those seeking flexibility, since benefits can be used for home care, assisted living, nursing facilities, or even informal care provided by family members.

Q: Does SecureCare IV cover home care and care provided by family members?

Yes. One of SecureCare IV’s most valuable features is its cash indemnity benefit, which allows policyholders to spend their monthly benefit however they choose after qualifying for long-term care benefits. This includes paying for professional home health care, modifying a home for accessibility, compensating family caregivers, or covering other qualified long-term care expenses. Unlike reimbursement-based policies, there is no requirement to submit invoices or prove exactly how every dollar is spent, giving families significantly greater flexibility when coordinating care.

Q: What are the new features introduced with SecureCare IV?

SecureCare IV builds upon previous versions by adding several meaningful enhancements. These include a new 20-pay premium option, retroactive payment of benefits after satisfying the 90-day elimination period, expanded international coverage that allows eligible policyholders to receive their full monthly benefit while living abroad, and a guaranteed death benefit that is at least equal to total premiums paid if death occurs before long-term care is needed. The policy also provides limited benefits for home modifications and caregiver training during the elimination period, helping families begin care sooner.

Q: What are the new features introduced with SecureCare IV?

SecureCare IV builds upon previous versions by adding several meaningful enhancements. These include a new 20-pay premium option, retroactive payment of benefits after satisfying the 90-day elimination period, expanded international coverage that allows eligible policyholders to receive their full monthly benefit while living abroad, and a guaranteed death benefit that is at least equal to total premiums paid if death occurs before long-term care is needed. The policy also provides limited benefits for home modifications and caregiver training during the elimination period, helping families begin care sooner.