Lincoln MoneyGuard Fixed Advantage Hybrid Life and Long Term Care Insurance Review – Long Term Care University

Long Term Care University – Question of the Month – 04/15/26

By Aaron Skloff, AIF, CFA, MBA

Q: We read the Long Term Care University article ‘Traditional Versus Hybrid Life and Long Term Care Insurance’ and prefer the Hybrid Long Term Care Insurance (LTC) policy. Can you please review the Lincoln MoneyGuard Fixed Advantage Hybrid Life and LTC policy?

Overview. Lincoln Financial Group is part of Lincoln National Corporation, an A.M. Best A rated company, founded in 1905. The Lincoln MoneyGuard III (3) policy is a Hybrid Life and Long Term Care Insurance (also called Combination or asset based) policy. With Traditional LTC policies, premiums can be increased and you may not receive any benefits if you do not need LTC. With Hybrid LTC policies the benefits and premiums are guaranteed. The insurance company either: 1) pays you if you need LTC, 2) pays your heirs if you do not need LTC, 3) pays you and your heirs if you need a modest amount of LTC or 4) pays you a refund if you cancel the policy.

Click Here for Your Long Term Care Insurance Quotes

Lincoln MoneyGuard Fixed Advantage is Unique Because It Does Not Have an Elimination Period for Home Care or Facility Care. Like a deductible on an automobile or homeowners insurance policy, an elimination period (EP) on a LTC insurance policy sets period you pay for your LTC costs out of your own pocket. With a zero day EP, you gain three advantages: 1) Zero or low out-of-pocket costs when your care begins, 2) Higher probability the insurance company will pay all of your LTC costs and 3) Zero or low probability you will need to liquidate assets (and have to pay the commissions, taxes and penalties associated with those liquidations) to pay for your care during your EP.

Lincoln MoneyGuard Fixed Advantage is Unique Because It Has the Benefit Transfer Rider (BTR). The BTR allows beneficiaries the option to leverage all or some of their death benefit proceeds to increase LTC benefits, death benefit and length of protection on their existing MoneyGuard Fixed Advantage policy with no additional underwriting requirements. LTC benefits are transferred to the beneficiary’s policy at a ratio equal to the beneficiary’s original LTC to premium ratio – increasing the Total LTC Benefit Limit (Pool), not the Monthly LTC benefit.

Lincoln MoneyGuard Fixed Advantage Policy Options. The policy options include: Benefit periods of 3-6 years; Inflation protection of none, 3% compound, and 5% compound; Elimination period of zero days; Reimbursement based benefit payment method; Flexible Care Cash Amendment pays 80% of the maximum daily benefit for home care (no receipts required) up to the death benefit limit; Terminal Illness rider; and a Residual life insurance benefit (even if you deplete of your LTC benefits) equal to the lesser of 5% of the face amount of insurance or $10,000.

Lincoln MoneyGuard Fixed Advantage Policy Premium Payment Options. They include: one time (single-pay) through 10 years (10-pay), based on age. Like buying a home, the longer your payment option, the higher your cumulative payments.

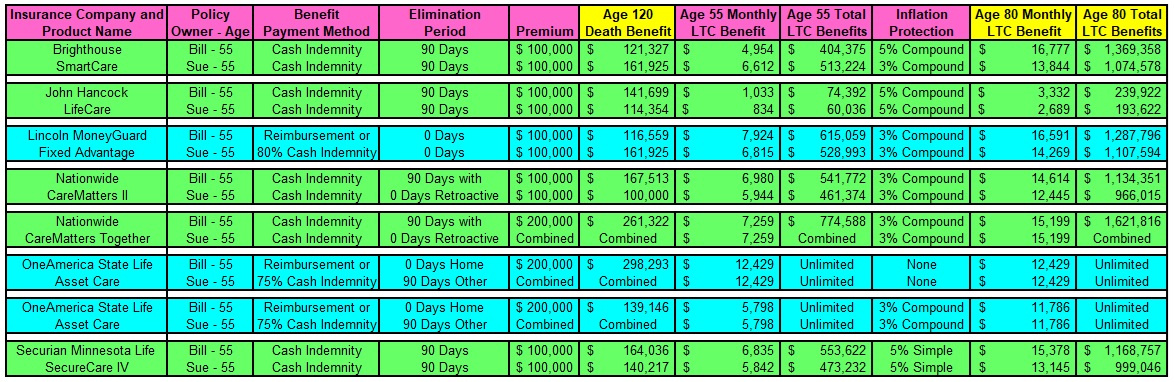

How Lincoln MoneyGuard Fixed Advantage Compares with Other Hybrid LTC Policies. Let’s look at a husband and wife, Bill and Sue, who are each 55 years old and reside in Maryland. They each pay a $100,000 one-time premium ($200,000 combined with Nationwide CareMatters Together and OneAmerica State Life Asset Care) and are expected to need LTC in 25 years at the age of 80. They are comparing Hybrid policies that offer the largest LTC benefits with inflation protection (unless noted). See reimbursement policies in blue and cash indemnity policies in green in the chart below.

Lincoln MoneyGuard Fixed Advantage Outperforms Competitors – with High Monthly and Total Benefits, and Zero Day Elimination Period. Bill will have $16,591 monthly and $1,287,796 total LTC benefits, while Sue will have $14,269 and $1,107,594, respectively. Brighthouse SmartCare is a strong cash indemnity alternative for Bill and Sue due to its high monthly and total LTC benefits, and its option to link policy values to major market indices. John Hancock LifeCare is notable for its option to link policy values to major market indices. Nationwide Care Matters II is a strong cash indemnity alternative for Bill and Sue due to its high monthly and total LTC benefits and its 90 day with zero day retroactive elimination period. Nationwide CareMatters Together is a strong cash indemnity alternative for Bill and Sue due to its high monthly LTC benefits and its 90 day with zero day retroactive elimination period. OneAmerica State Life Asset Care is a strong (partial cash indemnity) alternative due to its unlimited, lifetime total LTC benefits. Minnesota Life SecureCare IV is a strong cash indemnity alternative for Bill and Sue due to its higher monthly and total LTC benefits and its 90 day with zero day retroactive elimination period.

Click to Enlarge

Action Steps and Conclusions. Lincoln MoneyGuard Fixed Advantage provides high monthly and total LTC benefits, with a zero day elimination period. Since premiums vary greatly based on age, health and marital status, request individualized quotes.

Aaron Skloff, Accredited Investment Fiduciary (AIF), Chartered Financial Analyst (CFA) charter holder, Master of Business Administration (MBA), is the Chief Executive Officer of Skloff Financial Group, a Registered Investment Advisory firm. The firm specializes in financial planning and investment management services for high net worth individuals and benefits for small to middle sized companies. He can be contacted at www.skloff.com or 908-464-3060.

![]()

Click Here for Your Long Term Care Insurance Quotes

Frequently Asked Questions

Q: What is a hybrid life and long-term care insurance policy, and how does it differ from traditional policies?

A hybrid policy combines life insurance with long-term care (LTC) coverage into a single asset-based plan. Unlike traditional LTC policies, where premiums can increase over time and you risk losing your money if you never need care, a hybrid policy guarantees locked-in premiums and benefits. If you need long-term care, the policy pays out care benefits; if you never need care, it pays a tax-free death benefit to your heirs. Some policies also offer a partial death benefit if only a small amount of care is used, or a refund if you choose to cancel.

Q: What makes the elimination period unique under the Lincoln MoneyGuard Fixed Advantage plan?

The Lincoln MoneyGuard Fixed Advantage stands out because it features a zero-day elimination period for both home care and facility care. In traditional insurance terms, an elimination period acts like a deductible, requiring you to pay for your own care costs out-of-pocket for a set period (often 90 days) before policy payouts trigger. With a zero-day timeline, benefits begin immediately on day one of your care, preventing you from having to quickly liquidate personal retirement assets or face unexpected tax liabilities and penalties to cover early care bills.

Q: How does the Benefit Transfer Rider (BTR) work?

The Benefit Transfer Rider is a built-in feature that gives named beneficiaries the flexibility to redirect their inherited death benefit proceeds into their own existing MoneyGuard Fixed Advantage policies. Instead of taking a standard cash payout, a beneficiary can use those funds to automatically boost their own total LTC pool, death benefit, and duration of protection without having to go through any new medical underwriting. The funds transfer at a ratio mapped to the beneficiary’s original policy structure, expanding their long-term care pool rather than changing their monthly payout limit.

Q: What is the Flexible Care Cash Amendment, and how does it pay out?

The Flexible Care Cash feature modifies the policy’s standard reimbursement model into a more flexible cash-indemnity hybrid for home health care. This amendment allows policyholders to receive 80% of their maximum daily home care benefit directly in cash without needing to submit receipts or formal itemized bills. It is designed to smoothly cover informal care—such as paying unlicensed family members, neighbors, or friends to look after you at home—up to the limits of the policy’s face value.

Q: What are the premium payment options, and how do they impact overall cost?

Lincoln offers flexible payment structuring ranging from a single lump-sum premium (single-pay) up to a 10-year installment schedule (10-pay), depending on your age at purchase. Choosing a longer payment schedule provides greater short-term financial breathing room, but like financing a house, extending the timeframe results in a higher cumulative lifetime premium cost. Because rates and structures vary widely depending on your entry age, health, and marital status, customizing a payment plan with a financial professional is recommended.

Q: Does the policy offer any financial protection if I entirely deplete my long-term care benefits?

Yes, the policy includes a built-in Residual Life Insurance Benefit explicitly designed to preserve a legacy payout for your heirs even if you completely drain your pool of long-term care money. If severe, long-term chronic illness requires you to use every dollar allocated for medical and facility care, the policy still guarantees a small death benefit upon your passing. This residual payout is equal to the lesser of 5% of the policy’s original face amount or $10,000, ensuring your beneficiaries receive something.