Medicare Part B Premiums 2020

Click to Enlarge

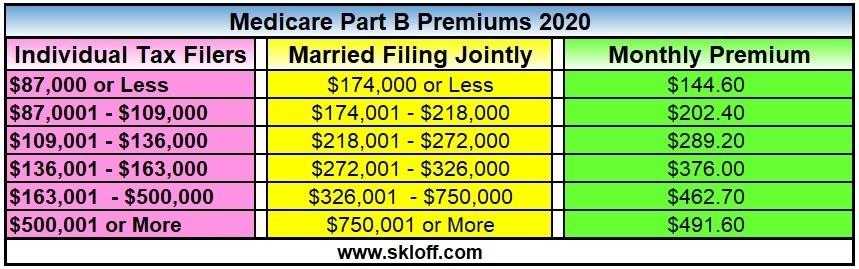

Part B premiums are based on tax returns from two years earlier.

Medicare doesn’t cover long-term care (also called custodial care).

Part B Deductible and Coinsurance

You pay $198 per year for your Part B deductible. After your deductible is met, you typically pay 20% of the Medicare-approved amount for these:

Most doctor services (including most doctor services while you’re a hospital inpatient)

Outpatient therapy

Durable medical equipment