John Hancock LifeCare Hybrid Life and Long Term Care Insurance Review – Long Term Care University

![]()

Long Term Care University – Question of the Month – 04/15/26

By Aaron Skloff, AIF, CFA, MBA

Q: We read the Long Term Care University article ‘Traditional Versus Hybrid Life and Long Term Care Insurance’ and prefer the Hybrid Long Term Care Insurance (LTC) policy. Can you please review the John Hancock LifeCare Hybrid LTC policy?

Overview. John Hancock, an A.M. Best A+ rated, founded in 1862. The John Hancock LifeCare policy is a Hybrid Life and Long Term Care Insurance (also called Combination or asset based) policy. With Traditional LTC policies, premiums can be increased and you may not receive any benefits if you do not need LTC. With Hybrid LTC policies the benefits and premiums are guaranteed. The insurance company either: 1) pays you if you need LTC, 2) pays your heirs if you do not need LTC, 3) pays you and your heirs if you need a modest amount of LTC or 4) pays you a refund if you cancel the policy.

Click Here for Your Long Term Care Insurance Quotes

John Hancock LifeCare is Unique Because it is a Cash Indemnity or Reimbursement Policy. There are two primary benefit payment methods among LTC policies. Reimbursement policies, the most common type of policies, require you to submit documentation of all expenses for reimbursement up to your monthly LTC benefits. Upon receipt of qualified expenses, John Hancock will pay up to the maximum monthly benefit amount, even if it exceeds the IRS per diem limit in the year. Cash Indemnity policies pay up to your monthly LTC benefits, regardless of your expenses, up to the IRS per diem limit in the year.

John Hancock LifeCare is Unique Because It is an Indexed Universal Life Insurance Policy Offering the Option to Link Policy Values to Major Market Indices. With most LTC policies you choose a fixed inflation protection growth rate (e.g.: 3% or 5% compound). With John Hancock LifeCare you can choose a fixed inflation protection of 5%, a fixed account with a minimum guaranteed rate of 1% or one linked to financial market indices (indexed). Benefit amounts have the potential to increase with market gains up to an annual maximum growth rate (cap) but will never drop below the policy’s original amounts. You can choose to track one or more of the S&P 500 Index (Select Capped or High Capped) or Barclays Global MA Index

John Hancock LifeCare. The policy options include: Benefit periods of 2, 4 or 6 years; Inflation protection of 5% compound or indexed; Elimination period of 90 days; Terminal illness benefit 50% of your policy’s face amount; Cash surrender value varies by benefit design and inflation protection option selected. John Hancock Vitality PLUS (Healthy Engagement Benefit rider) increase the policy’s death benefit and LTC benefit based on you taking healthy actions.

John Hancock LifeCare Policy Premium Payment Options. They include: one time (single-pay), 5-pay, 10-pay and 15-pay.

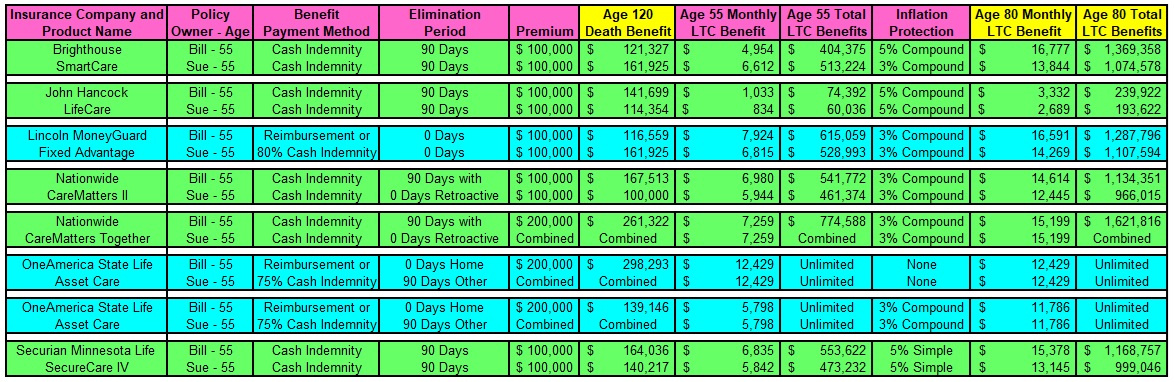

How John Hancock LifeCare Compares with Other Hybrid LTC Policies. Let’s look at a husband and wife, Bill and Sue, who are each 55 years old and reside in Maryland. They each pay a $100,000 one-time premium ($200,000 combined with Nationwide CareMatters Together and OneAmerica State Life Asset Care) and are expected to need LTC in 25 years at the age of 80. They are comparing Hybrid policies that offer the largest LTC benefits with inflation protection included in the premium (unless noted otherwise). They prefer Cash Indemnity (reimbursement policies in blue, cash indemnity policies in green in the chart below).

John Hancock LifeCare Underperforms Most Competitors on a Guaranteed Basis with Lower Monthly and Total LTC Benefits. Bill will have $3,572 monthly and $257,177 total LTC benefits, while Sue will have $2,960 and $213,113, respectively. Brighthouse SmartCare is a strong cash indemnity alternative for Bill and Sue due to its high monthly and total LTC benefits, and its option to link policy values to major market indices. Lincoln MoneyGuard Fixed Advantage is a strong (partial cash indemnity) alternative Bill and Sue due to its high monthly LTC benefits to its 0 day elimination period. Nationwide Care Matters II is a strong cash indemnity alternative for Bill and Sue due to its high monthly and total LTC benefits and its 90 day with zero day retroactive elimination period. Nationwide CareMatters Together is a strong cash indemnity alternative for Bill and Sue due to its high monthly LTC benefits and its 90 day with zero day retroactive elimination period. OneAmerica State Life Asset Care is a strong (partial cash indemnity) alternative due to its unlimited, lifetime total LTC benefits. Securian Minnesota Life SecureCare IV is a strong cash indemnity alternative for Bill and Sue due to its high monthly and total LTC benefits and its 90 day with zero day retroactive elimination period.

Click to Enlarge

Conclusions. John Hancock LifeCare provides low monthly and total LTC benefits and has the option to link policy values to market indices, with the flexibility of formal and informal care providers (including family and friends). Since premiums vary greatly based on age, health and marital status, request individualized quotes.

Aaron Skloff,, Accredited Investment Fiduciary (AIF), Chartered Financial Analyst (CFA) charter holder, Master of Business Administration (MBA), is the Chief Executive Officer of Skloff Financial Group, a Registered Investment Advisory firm. The firm specializes in financial planning and investment management services for high net worth individuals and benefits for small to middle sized companies. He can be contacted at www.skloff.com or 908-464-3060.

![]()

Click Here for Your Long Term Care Insurance Quotes

Frequently Asked Questions

Q: What is John Hancock LifeCare, in plain terms?

LifeCare is John Hancock’s current hybrid offering, combining an indexed universal life insurance policy with a long-term care benefit, so a single premium can ultimately pay out as LTC benefits, as a tax-free death benefit to heirs, or as some blend of the two if only modest care is ever used. It is built to give policyholders guaranteed coverage they cannot outlive, while also offering the flexibility to link a portion of policy values to market index performance rather than locking in one fixed crediting rate. Because it is issued as life insurance with attached LTC riders, it does not qualify as a state Long-Term Care Partnership policy, which is a distinction worth understanding if partnership-plan asset protection is part of the planning goal.

Q: How does LifeCare differ from the older John Hancock long-term care products advisors may remember?

John Hancock built its reputation decades ago as one of the largest sellers of traditional, stand-alone long-term care insurance, a book of business so large that the company still pays out several million dollars a day in claims to legacy policyholders. Roughly a decade ago, a prolonged low interest rate environment pushed John Hancock to stop selling new traditional LTC policies and pivot toward hybrid life insurance products with LTC riders instead. Those transitional rider-based UL policies, still marketed for a time afterward, were criticized for capping guarantees only through a certain mortality age and for shifting interest rate and cost-of-insurance risk onto the policyholder. LifeCare represents John Hancock’s newer attempt to fix that gap by wrapping LTC benefits into a policy structure designed to guarantee both premium and benefit for life.

Q: What are the biggest advantages and drawbacks of LifeCare according to independent reviewers?

Independent long-term care insurance reviewers point to several genuine strengths: deep institutional claims-paying experience, the optional Vitality wellness program that can add rewards for healthy habits, a flexible universal life chassis that allows adjustable premiums, and a guaranteed death benefit if care is never needed so the premium dollars are not simply lost. The same reviewers are equally direct about the tradeoffs, most notably that universal life products with LTC riders carry more moving parts than a simple fixed hybrid design, including cost-of-insurance charges and interest-crediting mechanics that take more effort to fully understand. That added complexity is generally the price of the extra flexibility and market-linked upside the product is built around.

Q: How do LifeCare’s guaranteed benefits stack up against competing hybrid policies?

When priced side by side against other single-premium hybrid designs for a same-age, same-state couple, LifeCare’s guaranteed monthly and lifetime LTC benefit figures have come in lower than several well-known competitors, including Brighthouse SmartCare, OneAmerica State Life Asset Care, and Nationwide’s CareMatters products. Those competing policies tend to differentiate themselves in different ways, such as larger guaranteed payouts, shorter or zero-day elimination periods, or unlimited lifetime benefit pools, while LifeCare’s differentiator is the option to link a portion of growth to market indices rather than a single fixed rate. For clients whose priority is the largest possible guaranteed LTC benefit for a given premium dollar, that tradeoff is worth running side by side before deciding.

Q: What does the real-world claims and service experience look like with John Hancock?

John Hancock services one of the largest blocks of in-force long-term care insurance in the country, and its scale is reflected in the sheer volume of daily claims payments it processes on legacy business. That scale, however, has come with mixed customer feedback in independently collected reviews, where some policyholders and their families have described slow reimbursement turnaround, cumbersome online claims portals, and difficulty reaching a live representative outside of formal complaint channels. This pattern is not unique to John Hancock among large LTC carriers, but it is a reasonable reason to ask any carrier being considered, including John Hancock, detailed questions about their claims process and reimbursement timelines before a policy is purchased.

Q: Who tends to be the best fit for a policy like LifeCare?

LifeCare and similar universal-life-based hybrid designs tend to appeal most to people who want meaningful life insurance protection alongside their long-term care benefit, are comfortable with a bit more product complexity in exchange for potential index-linked growth, and like the idea of wellness-program rewards for healthy behavior. It is generally a less natural fit for someone whose sole objective is maximizing the largest possible guaranteed monthly LTC benefit per premium dollar, since simpler fixed hybrid designs from other carriers have historically delivered more guaranteed benefit for the same premium in side-by-side comparisons. As with any hybrid LTC decision, the right answer depends heavily on age, health, marital status, and which single feature — guaranteed benefit size, death benefit, growth potential, or claims flexibility — matters most to the individual.