Brighthouse SmartCare Hybrid Life and Long Term Care Insurance Review – Long Term Care University

Long Term Care University – Question of the Month – 04/15/26

By Aaron Skloff, AIF, CFA, MBA

Q: We read the Long Term Care University article ‘Traditional Versus Hybrid Life and Long Term Care Insurance’ and prefer the Hybrid Long Term Care Insurance (LTC) policy. Can you please review the Brighthouse SmartCare Hybrid LTC policy?

Overview. Brighthouse Life Insurance Company, an A.M. Best A rated, founded in 2017 (originating from Travelers and MetLife). The Brighthouse SmartCare policy is a Hybrid Life and Long Term Care Insurance (also called Combination or asset based) policy. With Traditional LTC policies, premiums can be increased and you may not receive any benefits if you do not need LTC. With Hybrid LTC policies the benefits and premiums are guaranteed. The insurance company either: 1) pays you if you need LTC, 2) pays your heirs if you do not need LTC, 3) pays you and your heirs if you need a modest amount of LTC or 4) pays you a refund if you cancel the policy.

Click Here for Your Long Term Care Insurance Quotes

Brighthouse SmartCare is Unique Because it is a Cash Indemnity Policy. There are two primary benefit payment methods among LTC policies. Reimbursement policies, the most common type of policies, require you to submit documentation of all expenses for reimbursement up to your monthly LTC benefits. Cash Indemnity policies pay up to your monthly LTC benefits, regardless of your expenses.

Brighthouse SmartCare is Unique Because It is an Indexed Universal Life Insurance Policy Offering the Option to Link Policy Values to Major Market Indices. With most LTC policies you choose a fixed inflation protection growth rate (e.g.: 3% or 5% compound). With Brighthouse SmartCare you can choose a fixed inflation protection or one linked to a financial market indices (indexed). Benefit amounts have the potential to increase with market gains up to an annual maximum growth rate (cap) but will never drop below the policy’s original amounts. You can choose to track one or more of the following indices: S&P 500 Index, Russell 2000 Index, or MSCI EAFE Index.

Brighthouse SmartCare Policy Options. The policy options include: Benefit periods of 4 or 6 yearss; Inflation protection growth rate (e.g.: 3% or 5% compound). With Brighthouse SmartCare you can choose a fixed inflation protection or one linked to a financial market indices (indexed). Benefit amounts have the potential to increase with market gains up to an annual maximum growth rate (cap) but will never drop below the policy’s original amounts. You can choose to track one or more of the following indices: S&P 500 Index, Russell 2000 Index, or MSCI EAFE Index.

Brighthouse SmartCare Policy Options. The policy options include: Benefit periods of 4 or 6 years; Inflation protection of none, 5% compound or indexed;

Elimination period of 90 days; Terminal illness benefit at the lesser of $250,000 or 50% of your policy’s face amount; Cash surrender value varies by benefit design and inflation protection option selected. International Benefits are 100% of monthly maximum LTC benefits for the entire benefit period (e.g.: 6 years).

Brighthouse SmartCare Policy Premium Payment Options. They include: one time (single-pay), 2 year, 3 years, 4 years, 5 years and 10 years (10-pay). Like buying a home, the longer your payment option, the higher your cumulative payments (except for the 2-pay).

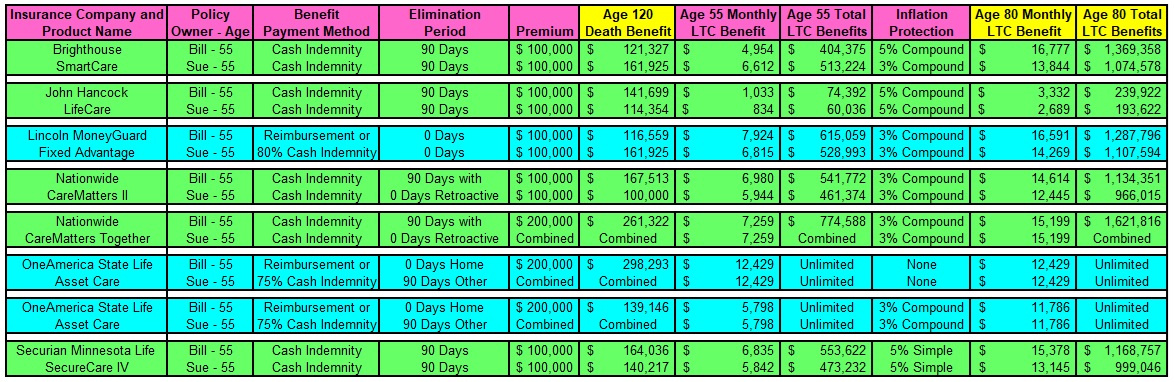

How Brighthouse SmartCare Compares with Other Hybrid LTC Policies. Let’s look at a husband and wife, Bill and Sue, who are each 55 years old and reside in Maryland. They each pay a $100,000 one-time premium ($200,000 combined with Nationwide CareMatters Together and OneAmerica State Life Asset Care) and are expected to need LTC in 25 years at the age of 80. They are comparing Hybrid policies that offer the largest LTC benefits with inflation protection included in the premium (unless noted otherwise). They prefer Cash Indemnity (reimbursement policies in blue, cash indemnity policies in green in the chart below).

Brighthouse SmartCare Outperforms Most Competitors on a Guaranteed Basis with Higher Monthly and Total LTC Benefits. Bill will have $16,777 monthly and $1,369,358 total LTC benefits, while Sue will have $13,844 and $1,074,578, respectively. John Hancock LifeCare is notable for its option to link policy values to major market indices. Lincoln MoneyGuard Fixed Advantage is a strong (partial cash indemnity) alternative Bill and Sue due to its high monthly LTC benefits to its 0 day elimination period. Nationwide Care Matters II is a strong cash indemnity alternative for Bill and Sue due to its high monthly and total LTC benefits and its 90 day with zero day retroactive elimination period. Nationwide CareMatters Together is a strong cash indemnity alternative for Bill and Sue due to its high monthly LTC benefits and its 90 day with zero day retroactive elimination period. OneAmerica State Life Asset Care is a strong (partial cash indemnity) alternative due to its unlimited, lifetime total LTC benefits. Securian Minnesota Life SecureCare IV is a strong cash indemnity alternative for Bill and Sue due to its higher monthly and total LTC benefits and its 90 day with zero day retroactive elimination period.

Click to Enlarge

Conclusions. Brighthouse SmartCare provides high monthly and total LTC benefits and has the option to link policy values to market indices, with the flexibility of formal and informal care providers (including family and friends). Since premiums vary greatly based on age, health and marital status, request individualized quotes.

Aaron Skloff, Accredited Investment Fiduciary (AIF), Chartered Financial Analyst (CFA) charter holder, Master of Business Administration (MBA), is the Chief Executive Officer of Skloff Financial Group, a Registered Investment Advisory firm. The firm specializes in financial planning and investment management services for high net worth individuals and benefits for small to middle sized companies. He can be contacted at www.skloff.com or 908-464-3060.

![]()

Click Here for Your Long Term Care Insurance Quotes

Frequently Asked Questions

Q: What is the Brighthouse SmartCare policy?

A: Brighthouse SmartCare is a Hybrid (also called Combination or asset-based) Life and Long Term Care Insurance policy offered by Brighthouse Life Insurance Company, an A.M. Best A rated insurer founded in 2017 that originated from Travelers and MetLife. Unlike Traditional Long Term Care policies, where premiums can increase over time and you may receive no benefit at all if you never need care, Brighthouse SmartCare guarantees both premiums and benefits. Under the policy, the insurance company will pay you if you need Long Term Care, pay your heirs a death benefit if you do not need Long Term Care, pay a combination of both you and your heirs if you need only a modest amount of care, or refund your premium if you cancel the policy.

Q: What makes Brighthouse SmartCare a Cash Indemnity policy, and why does that matter?

A: Brighthouse SmartCare is a Cash Indemnity policy, meaning it pays you up to your full monthly Long Term Care benefit regardless of your actual expenses, with no requirement to submit receipts or documentation for reimbursement. This differs from the more common Reimbursement policies, which require you to submit documentation of all care-related expenses before the insurer reimburses you up to your monthly benefit. The Cash Indemnity structure gives policyholders more flexibility and simplicity in how benefits are received and used.

Q: What makes Brighthouse SmartCare an Indexed Universal Life Insurance policy?

A: Brighthouse SmartCare is built on an Indexed Universal Life Insurance chassis, which means policyholders can link their policy values to the performance of major market indices rather than choosing only a fixed inflation protection growth rate. Most Long Term Care policies simply offer a fixed compound growth rate, such as 3% or 5%, but Brighthouse SmartCare allows you to choose fixed inflation protection or an indexed option tied to market performance. This gives the policy potential upside that fixed-rate designs do not offer.

Q: Which market indices can be linked to a Brighthouse SmartCare policy, and is there downside risk?

A: Policyholders can choose to track one or more of the S&P 500 Index, the Russell 2000 Index, or the MSCI EAFE Index for the indexed inflation protection option. Benefit amounts have the potential to increase with market gains up to an annual maximum growth rate, known as a cap, but importantly the benefit amounts will never drop below the policy’s original amounts even if the linked index declines. This structure lets policyholders participate in market upside for their Long Term Care benefits while being protected from downside index performance.

Q: What benefit period options are available under Brighthouse SmartCare?

A: Brighthouse SmartCare offers Long Term Care benefit periods of either 4 or 6 years. The benefit period you select, combined with your chosen inflation protection option, directly affects both your monthly and total available Long Term Care benefits, so this choice should be made carefully in the context of your overall planning goals.

Q: What inflation protection options does Brighthouse SmartCare offer?

A: Policyholders can choose among no inflation protection, a 5% compound fixed growth rate, or an indexed option linked to major market indices. The indexed option allows benefit amounts to potentially grow with market gains, subject to an annual cap, while still guaranteeing that benefits never fall below their original amount. Selecting the right inflation protection option is important because Long Term Care costs paid for by the policy may not be needed for many years, and inflation can meaningfully erode the purchasing power of a fixed benefit over that time.

Q: What is the elimination period under Brighthouse SmartCare?

A: Brighthouse SmartCare has a 90-day elimination period, which is the waiting period after you qualify for benefits before the policy begins paying for Long Term Care expenses. This is a standard elimination period length in the Hybrid Long Term Care marketplace, though it is longer than some competing policies that offer a 90-day elimination period with zero-day retroactive coverage, or even a 0-day elimination period.

Q: Does Brighthouse SmartCare include a terminal illness benefit?

A: Yes, Brighthouse SmartCare includes a terminal illness benefit equal to the lesser of $250,000 or 50% of the policy’s face amount. This benefit allows policyholders diagnosed with a terminal illness to access a portion of their death benefit while still living, providing additional financial flexibility during a difficult time.

Q: Does Brighthouse SmartCare provide international Long Term Care benefits?

A: Yes, Brighthouse SmartCare provides international benefits equal to 100% of the monthly maximum Long Term Care benefit for the entire benefit period, such as the full 6 years if that benefit period is selected. This is a notable feature for policyholders who travel frequently or may split time living outside the United States and want assurance that their Long Term Care coverage will still apply abroad.

Q: What premium payment options are available for Brighthouse SmartCare?

A: Brighthouse SmartCare offers several premium payment options, including a one-time single-pay premium, as well as 2-year, 3-year, 4-year, 5-year, and 10-year (10-pay) payment schedules. Choosing a payment option is similar to choosing a mortgage term: as with buying a home, the longer your payment option, the higher your cumulative payments tend to be, with the notable exception of the 2-pay option.

Q: How does Brighthouse SmartCare compare to other Hybrid Long Term Care policies?

A: In a comparison of a 55-year-old husband and wife in Maryland each paying a $100,000 one-time premium and expected to need care at age 80, Brighthouse SmartCare outperformed most competitors on a guaranteed basis, providing the husband with $16,777 in monthly and $1,369,358 in total Long Term Care benefits, and the wife with $13,844 in monthly and $1,074,578 in total benefits. Strong alternatives in the same comparison included John Hancock LifeCare, notable for also linking policy values to market indices; Lincoln MoneyGuard Fixed Advantage, notable for its 0-day elimination period; Nationwide CareMatters II and Nationwide CareMatters Together, both notable for high benefits paired with a 90-day, zero-day-retroactive elimination period; OneAmerica State Life Asset Care, notable for unlimited lifetime total benefits; and Securian Minnesota Life SecureCare IV, notable for higher monthly and total benefits with the same favorable elimination period structure.

Q: Who should consider a Brighthouse SmartCare policy?

A: Brighthouse SmartCare is well suited to individuals and couples who want high guaranteed monthly and total Long Term Care benefits, prefer the simplicity of Cash Indemnity claims payments over reimbursement-based claims, and want the option to link their benefit growth to market index performance rather than settling for a fixed growth rate alone. It also appeals to those who value flexibility in how and where care is delivered, including the use of formal and informal caregivers such as family and friends, and international coverage for those who travel or live abroad. Because premiums vary significantly based on age, health, and marital status, individuals considering this policy should request individualized quotes before making a decision.